It's Time for Real Assets

Private debt1 can be a lower-risk, higher-yielding alternative to traditional bonds

Key Takeaways:

- Private debt comprises loans to companies, infrastructure projects and real estate, and aircraft financing. The asset class benefits from a low-risk profile, low correlation to bond markets and backing by tangible assets.

- The private debt team at Natixis Global Asset Management is composed of professionals from four affiliates: Natixis Asset Management, AEW, Loomis Sayles and Mirova.

- Private debt is likely to appeal to a range of investors with long-term investment outlooks or long-term liabilities and who are in a position to benefit from illiquidity premia.

Resources

This shift is based on three trends which have gained rapid momentum in the post-financial crisis period. First, banks are progressively reducing their balance sheet exposure to credit amid Basel III regulatory requirements. Second, European borrowers are increasingly diversifying their sources of financing to reduce their reliance on banks. Third, European borrowers with capital expenditure needs and renewed appetite for overseas expansion are seeking to take advantage of historically low interest rates.

As rates fall, investors have lent capital in increasing volumes, driving down rates even further.

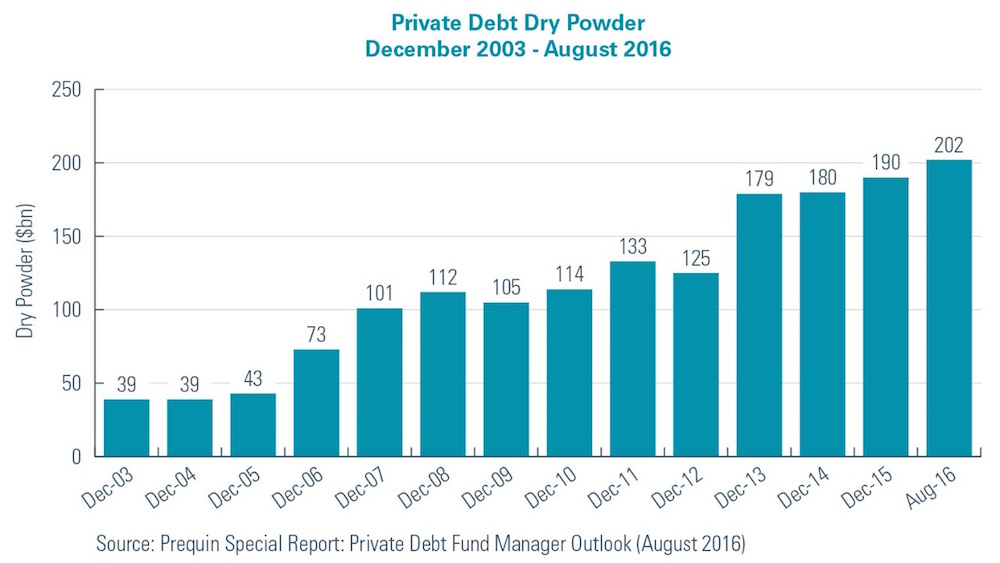

Yields on both government and corporate debt are now at levels that may no longer justify the risks taken. This has thrown the spotlight on the private debt industry, a niche sector with little media and advisor exposure, and fewer market participants than bond markets. Although private debt features in far fewer investment portfolios than bonds, it is steadily gaining ground, with private debt dry powder increasing fivefold between 2003 and August 2016.

New solution for a modern challenge

Institutional investors’ needs have coalesced in recent times around the same themes. Two Natixis surveys in 20152,3 found that investors’ preoccupations centred on high correlations between bonds and equities, ongoing low yields and high volatility. In essence, investors are signalling that they need new solutions for an investment environment that they view as unlikely to improve.

While private debt is not a new concept, its deployment is growing as changes in the real economy have made it more accessible to investors. Some investors have already seized the opportunity, viewing debt as an alternative or a complement to long-term bonds. They are attracted by the relatively low risks associated with most private debt – it is backed by tangible assets and has limited default rates and high recovery rates.

Because private debt markets have large and expanding volumes, global private debt managers with wide-ranging research and execution skills can achieve strong portfolio diversification effects. Portfolios can be diversified by geography and also by industry and sector, with private debt assets varying by their risk profiles and maturities.

The low-risk nature of private debt, its low correlation to other assets and its average yield of 2.5%-3% above Euribor4, has started to make the asset class compelling for investors with longer-term investment horizons.

Private debt in action

So what forms can private debt take? Private debt is effectively investing in real assets. It is the financing through loans or bonds of junior or senior projects. Investments in the real economy include loans to companies, to infrastructure projects, to real estate and for financing the building and maintenance of aircraft fleets.

There is virtually no limit to real asset financing possibilities, meaning the private debt sector has huge potential for growth and the addition of new asset types. More than $100bn of real estate private debt was issued last year, while infrastructure private debt issuance was $250bn and aircraft financing was $100bn.

Selecting loans, managing them securely

Financial expertise and knowledge of the market and its participants can provide privileged access to primary and secondary market data, which is important for sourcing loans. These loans must match portfolio guidelines and should offer the best potential risk-reward profile.

The process begins with analysis and the investment decision. Credit analysis involves a number of steps, including assessment of the borrower, the industry, capital structure, covenants and of recovery prospects.

After the investment decision has been executed, the next phase in producing consistent returns is monitoring. This phase includes asset and portfolio review, regular updates of the watch list and frequent discussions of potential disposals, amendments and waivers.

The strategy is predicated on strong investment discipline to mitigate the capital loss risk. Every investment carries risk, but the way an investment is structured and monitored can greatly minimise this risk. In the case of private debt, the investment is accompanied by substantial documentation, considerable due diligence and, sometimes, a specified cap on liabilities in the case of the loan not performing. Private debt is also backed by a tangible asset, so in the worst case scenario, if the debt is underperforming, the asset can be sold and the proceeds remitted to the debt holder.

A mix of skills is required

The key to being able to do all this and to successfully managing a private debt strategy is by combining different and complementary types of expertise. It is about allying disciplined portfolio management to knowledge of how to finance real economy projects. These skills are rarely found and combined under one roof.

The private debt management team at Natixis, for instance, is integrated into Natixis Global Asset Management (NGAM), with professionals at four NGAM affiliates - Natixis Asset Management, AEW, Loomis Sayles and Mirova - involved at each step of the asset acquisition, management, analysis and control processes.

Each affiliate has its own team of specialised portfolio managers, mainly former bankers with comprehensive experience in the relevant markets. Bank financing expertise - which is in the DNA of Natixis – is essential for analysing corporates and borrowers, while leveraging contacts among both constituents. The structuring and analysis of private debt deals - from corporate and real estate loans to infrastructure debt - requires deep knowledge and resources. NGAM’s private debt team can draw on the experience of over 50 investment experts, including 18 portfolio managers, 32 credit analysts and 4 financial engineers5.

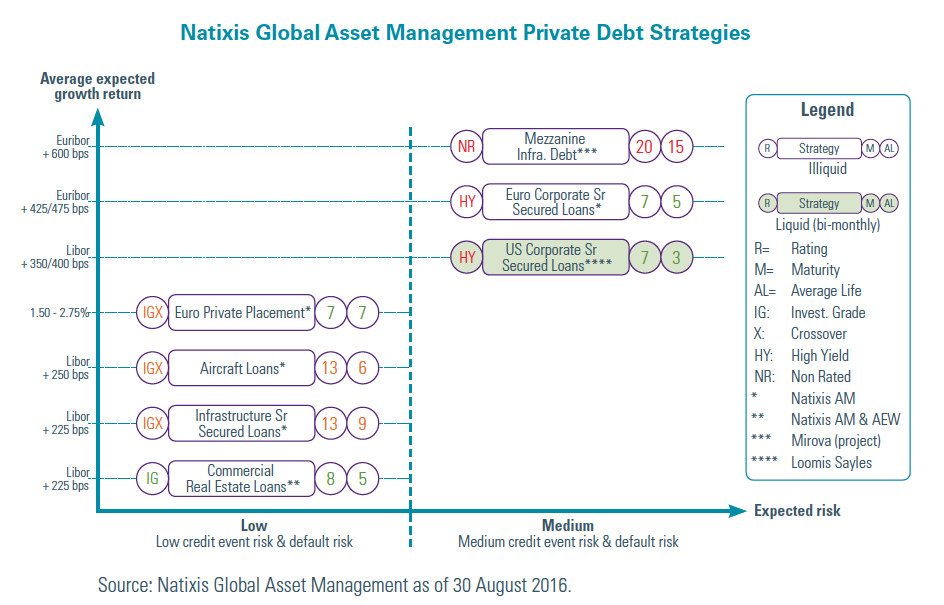

Risk analysis is the key to selection of assets and in the monitoring of the portfolios. NGAM’s private debt affiliates provide tailor-made investment solutions through dedicated funds or mandates investing in a wide range of strategies, including: commercial real estate loans, infrastructure senior secured loans, aircraft loans, euro private placement, US and Euro corporate senior secured loans and mezzanine infrastructure debt. All these strategies have a different risk-return profile depending on the rating of the underlying, the maturity of the loans and the expected risk (credit and default) that allow our affiliates to match the different expected returns of institutional investors.

On specific projects, unique partnerships between NGAM specialised affiliates can arise. This is the case in the commercial real estate strategy where each affiliate has complementary core skills: AEW Europe in real estate, and Natixis AM in structured credit management.

This allows NGAM to offer institutional investors the best of both affiliates: a combination of credit and real estate expertise.

Using this combination of expertise, the strategy can be tailored to focus on a specific sector, region or currency, or take a global market approach. Private debt is a key plank of NGAM’s overall strategy and each affiliate benefits from considerable support to develop their capabilities in this asset class as it moves from a peripheral to a core institutional allocation.

Who should be interested?

Private debt is likely to appeal to a range of investors with a long-term investment outlook or long-term liabilities and who are in a position to benefit from illiquidity premia.

For pension funds, private debt could form part of their asset-liability management efforts. They are typically heavily exposed to bonds, particularly government bonds with historically low yields, and seek alternative sources of yield with low risk and long-term consistency of returns. Private debt offers yield pick-up versus government bonds, and can also help provide inflation and interest rate protection.

In the insurance space, investment is increasingly guided by Solvency II requirements. Private debt carries a substantially lower capital charge than private equity, for example, enabling insurers investing in private debt to potentially increase yields from their fixed income allocation.

Private debt, with its rising volumes and deep pools of assets, is also attractive to many sovereign wealth funds. The exposure to real assets can or, in the case of oil producers, can be a natural hedge for oil prices. In some countries, sovereign wealth funds are incentivised to invest in local real assets, so they require an investment provider with knowledge of the sovereign wealth fund’s country and region.

For some investors, the private debt story is just beginning. For more experienced investors, it is getting more exciting and more rewarding.

2 Source: Natixis Global Asset Management 2015 Global Survey of Institutional Investors

3 Source: Natixis Global Asset Management 2015 Insurance Survey: Insights from Key Industry Decision Makers

4 Source : Natixis Global Asset Management, as of 30 August 2016

5 Source : Natixis Global Asset Management, as of 16/03/2016

Published in September 2016.

Natixis Global Asset Management S.A.

RCS Paris 453 952 681

Share Capital: €156 344 050

21 quai d’Austerlitz, 75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2016 NATIXIS GLOBAL ASSET MANAGEMENT S.A. – All rights reserved

Real Estate Debt

Real Estate Debt

Alternative Strategies May Add Value to Institutional Portfolios

Alternative Strategies May Add Value to Institutional Portfolios