Are Your Leveraged Loans Performing?

Amid high market stress robust strategies can continue to deliver.

Only in years like 2020 does it become clear which investment strategies are resilient and which are largely dependent on the tide which floats all boats. The leveraged loan market is a case in point. Returns have been excellent across the market for many years. But in times of stress, the rigour of the asset selection and the skill of the investment manager suddenly becomes paramount.

2 Source: MV Credit, data as of 31 March 2020

Published in May 2020

MV Credit Partners LLP

Registered Number : OC397214

Authorised and Regulated by the Financial Conduct Authority (FCA) with the FCA register number 67717.

45 Old Bond Street

London W1S 4QT

www.mvcredit.com

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2020 Natixis Investment Managers S.A. – All rights reserved

Highlights

- The rigour of asset selection in the leveraged loan market and the skill of the investment manager becomes paramount when the business environment is stressed.

- Sector and company selection, as well as the country in which companies operate, determine how robust a subordinated debt portfolio is.

- Experience and know-how of investment teams is critical. Experience of managing through difficult times leads to faster reactivity, while loan impairment is reduced by market knowledge and working with private equity sponsors who collaborate.

Resources

Subordinated debt: an investment success story

Leveraged loans, or subordinated debt, have provided strong returns to investors over a long period. These loans underpin private equity transactions, forming the debt component of a deal to buy a company, and complementing the riskier equity component injected by the private equity sponsor.

Over the long term, leveraged loans have the most predictable, consistent performance across the debt universe. They have returned more than senior corporate debt, high yield, REITS and infrastructure debt in terms of returns versus volatility.

Investors don’t need to wait as long as private equity investors to receive cash from their invested capital. Subordinated debt investors receive regular coupon payments from the moment a deal is completed, which is an effective derisking tool. And while funds are closed-ended and investors’ money is in theory locked up for up to 10 years, in practice private equity-owned companies often refinance or are sold so investors receive their capital back long before the 10 years is up.

Entering 2020, the whole private equity industry was in better shape than in the years leading up to the financial crisis. Sponsors have focused less on financial structuring, instead refining the business models of portfolio companies, and building business platforms to leverage resources across portfolios. So companies are leaner and less leveraged than in 2008. This, in a normal market environment, leaves leveraged loan investors sitting pretty.

Market-leading companies with low exposure to cycles

The trouble is, of course, this is no normal market. The resilience of loan portfolios is being severely tested in the current environment. Sector and company selection, even the jurisdiction in which companies operate, will all help determine how robust the subordinated debt portfolio really is.

“We create portfolios that navigate through cycles,” says Francois Decoeur, portfolio manager for MV Credit’s subordinated debt funds. “We invest in companies that can both grow in upmarkets and also weather choppy markets.”

MV Credit, an affiliate of Natixis Investment Managers, provides the financing for private deals where the target company is a leader in its national or regional sector, enabling it to retain market share and negotiate with suppliers and customers when the going gets tough. These companies often have diversified business channels which sustain revenues across the economic cycles. In addition, the companies are mainly based in northern Europe, where economies and political regimes are relatively stable.

Loans to healthcare companies are a prime example of countercyclical investments. MV Credit has high portfolio allocations to companies with market-leading medical technologies, such as diagnostics. It is also overweight on the business services sector, especially software companies which have recurring sales from a large client base of SMEs. The ability to model revenues of software companies from year to year is particularly attractive, allowing subordinated debt providers to accurately future cash generation deep into the future.

Sectors such as healthcare and business services are subject to long-term, non-cyclical trends, which means their business models should be able to withstand even severe downturns.

These attributes stand in contrast to, say, traditional manufacturing industries which are GDP-driven and exposed to capital expenditure cycles which can impact cashflows. When the pressure hits the topline, these kinds of companies will struggle to generate sufficient cash to pay all of their creditors.

“The impact on our portfolio has been well contained in the first wave of the pandemic,” says Decoeur, “We don’t invest in fashion, retail, automotive and so on, so we are not highly exposed to the cycle.”

Choose your partner with care

The resilience of leveraged loans is also predicated on the experience and know-how of investment teams. The experience of managing through difficult times can lead to faster reactivity. Know-how is about working with key private equity sponsors to access the best deals. Know-how also means partnering with sponsors who understand that a deal is a collaboration and who take the interests of all investors into account when making tough decisions.

“We were founded in 2000 and we work exclusively with private equity firms,” says Decoeur. MV Credit has provided €5.8bn of finance since it launched and has one of the longest-established credit management teams in the industry. “We have learned not only to select the right deals and good owners of companies, but also private equity sponsors who react well when there are difficulties in the portfolio.”

Private equity houses which have invested through many cycles and are used to dealing with distressed situations are likely to be more measured in their approach to their portfolio companies and to creditors. MV Credit therefore looks for private equity partners who signal early when company fundamentals are deteriorating, communicate well with other partners in the deal and, crucially, have the business skills and financial means to provide support to underlying companies when necessary.

“We won’t work with all private equity firms,” adds Decoeur. “We think sponsor selection is one of the reasons our portfolio is holding up in difficult times.”

The advantages of being sole lender

Some private equity deals are financed by a number of lenders. That can work well to get bigger deals done and to get access to complementary skills. But in times of trouble it can be beneficial to be the sole lender. “We are usually the sole lender or, sometimes, one of a small number of lenders,” says Decoeur. “When a portfolio company hits trouble, the fewer people you need to deal with, the easier it is to find a solution.”

Being a sole lender can be better in normal business environments too. It can speed conversations and decisions about key corporate actions such as refinancing, expansions, mergers and sponsor exits.

Simpler relationships that eschew the complexity of multiple partner structures can also lead to increased deal opportunities. “Having continuous contact with a number of trusted private equity sponsors means we often get first sight of deals that are not visible to the rest of the market,” says Decoeur. Equally, it allows MV Credit, using its own research and insight, to suggest specific funding deals to private equity sponsors. The result is more deals, better deals and more diversification in the loan portfolio.

ESG for downside protection

ESG integration can make a leveraged loan portfolio more robust. The willingness to decline a deal or divest if a portfolio company breaches core ESG values can mitigate losses. The risk that regulation will force a company to rectify poor environmental practices, the risk of controversies such as lawsuits and financial penalties, and the risk to workers and company reputation of unsafe working conditions can all impair loans.

“Put simply, if a business does not have a good sustainable profile it is a higher credit risk,” says Decoeur. MV Credit may be satisfied with a company’s fundamentals, the credentials of a company’s management, the structure of the deal and the valuation, but will not commit capital because key commercial practices are not sustainable.

And while MV Credit is attracted to the financial risk-return profile of the healthcare sector, it doesn’t invest in care homes, for instance. It believes that businesses that have a critical role in economy and society should not be subject to the profit motive.

Conclusion: surviving market stress

Leveraged loans are, historically speaking a high-performing asset class. But in times of high market stress only the most robust strategies will continue to deliver market-beating returns. More resilient strategies focus on less-cyclical businesses and use experience and knowhow to work with partners to avoid significant loan impairment.

“We have been in this market, and only this market, for 20 years,” notes Decoeur. “We have employed the same investment strategy that whole time. The only difference between now and then is we have a lot more experience.”

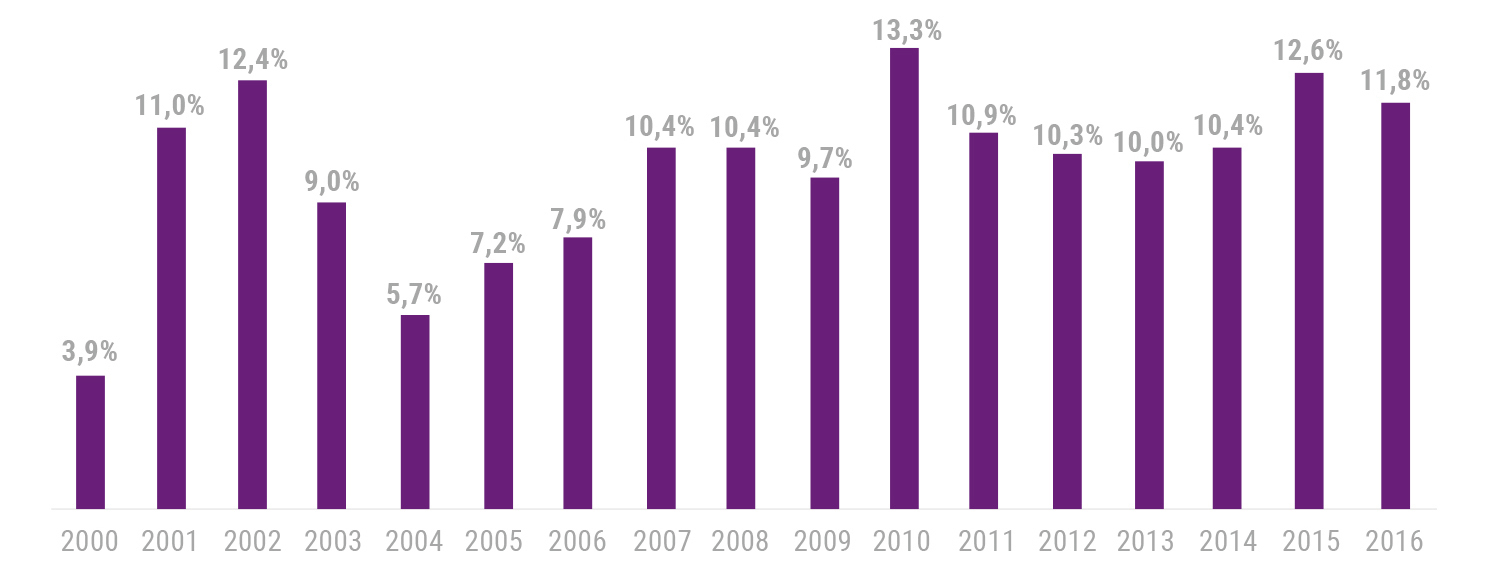

Leveraged loans, or subordinated debt, have provided strong returns to investors over a long period. These loans underpin private equity transactions, forming the debt component of a deal to buy a company, and complementing the riskier equity component injected by the private equity sponsor.

Over the long term, leveraged loans have the most predictable, consistent performance across the debt universe. They have returned more than senior corporate debt, high yield, REITS and infrastructure debt in terms of returns versus volatility.

Subordinated Debt Funds Average Returns1

1 Source: MV Credit, CEPRES. Data retrieved November 2019. Based on annualised realised default and loss rates of all European subordinated debt within: Computer/Technology, Healthcare, Consumer Industry, Industrials, Others/Unspecifed, Financials with investment year 2001-2019. Realised investments only. Sponsored investments only. Data period from 2001-2019. 2017 – 2019 data not available/not meaningful. Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of future results.

Investors don’t need to wait as long as private equity investors to receive cash from their invested capital. Subordinated debt investors receive regular coupon payments from the moment a deal is completed, which is an effective derisking tool. And while funds are closed-ended and investors’ money is in theory locked up for up to 10 years, in practice private equity-owned companies often refinance or are sold so investors receive their capital back long before the 10 years is up.

Entering 2020, the whole private equity industry was in better shape than in the years leading up to the financial crisis. Sponsors have focused less on financial structuring, instead refining the business models of portfolio companies, and building business platforms to leverage resources across portfolios. So companies are leaner and less leveraged than in 2008. This, in a normal market environment, leaves leveraged loan investors sitting pretty.

Market-leading companies with low exposure to cycles

The trouble is, of course, this is no normal market. The resilience of loan portfolios is being severely tested in the current environment. Sector and company selection, even the jurisdiction in which companies operate, will all help determine how robust the subordinated debt portfolio really is.

“We create portfolios that navigate through cycles,” says Francois Decoeur, portfolio manager for MV Credit’s subordinated debt funds. “We invest in companies that can both grow in upmarkets and also weather choppy markets.”

MV Credit, an affiliate of Natixis Investment Managers, provides the financing for private deals where the target company is a leader in its national or regional sector, enabling it to retain market share and negotiate with suppliers and customers when the going gets tough. These companies often have diversified business channels which sustain revenues across the economic cycles. In addition, the companies are mainly based in northern Europe, where economies and political regimes are relatively stable.

Loans to healthcare companies are a prime example of countercyclical investments. MV Credit has high portfolio allocations to companies with market-leading medical technologies, such as diagnostics. It is also overweight on the business services sector, especially software companies which have recurring sales from a large client base of SMEs. The ability to model revenues of software companies from year to year is particularly attractive, allowing subordinated debt providers to accurately future cash generation deep into the future.

Sectors such as healthcare and business services are subject to long-term, non-cyclical trends, which means their business models should be able to withstand even severe downturns.

These attributes stand in contrast to, say, traditional manufacturing industries which are GDP-driven and exposed to capital expenditure cycles which can impact cashflows. When the pressure hits the topline, these kinds of companies will struggle to generate sufficient cash to pay all of their creditors.

“The impact on our portfolio has been well contained in the first wave of the pandemic,” says Decoeur, “We don’t invest in fashion, retail, automotive and so on, so we are not highly exposed to the cycle.”

Choose your partner with care

The resilience of leveraged loans is also predicated on the experience and know-how of investment teams. The experience of managing through difficult times can lead to faster reactivity. Know-how is about working with key private equity sponsors to access the best deals. Know-how also means partnering with sponsors who understand that a deal is a collaboration and who take the interests of all investors into account when making tough decisions.

“We were founded in 2000 and we work exclusively with private equity firms,” says Decoeur. MV Credit has provided €5.8bn of finance since it launched and has one of the longest-established credit management teams in the industry. “We have learned not only to select the right deals and good owners of companies, but also private equity sponsors who react well when there are difficulties in the portfolio.”

Private equity houses which have invested through many cycles and are used to dealing with distressed situations are likely to be more measured in their approach to their portfolio companies and to creditors. MV Credit therefore looks for private equity partners who signal early when company fundamentals are deteriorating, communicate well with other partners in the deal and, crucially, have the business skills and financial means to provide support to underlying companies when necessary.

“We won’t work with all private equity firms,” adds Decoeur. “We think sponsor selection is one of the reasons our portfolio is holding up in difficult times.”

The advantages of being sole lender

Some private equity deals are financed by a number of lenders. That can work well to get bigger deals done and to get access to complementary skills. But in times of trouble it can be beneficial to be the sole lender. “We are usually the sole lender or, sometimes, one of a small number of lenders,” says Decoeur. “When a portfolio company hits trouble, the fewer people you need to deal with, the easier it is to find a solution.”

Being a sole lender can be better in normal business environments too. It can speed conversations and decisions about key corporate actions such as refinancing, expansions, mergers and sponsor exits.

Simpler relationships that eschew the complexity of multiple partner structures can also lead to increased deal opportunities. “Having continuous contact with a number of trusted private equity sponsors means we often get first sight of deals that are not visible to the rest of the market,” says Decoeur. Equally, it allows MV Credit, using its own research and insight, to suggest specific funding deals to private equity sponsors. The result is more deals, better deals and more diversification in the loan portfolio.

ESG for downside protection

ESG integration can make a leveraged loan portfolio more robust. The willingness to decline a deal or divest if a portfolio company breaches core ESG values can mitigate losses. The risk that regulation will force a company to rectify poor environmental practices, the risk of controversies such as lawsuits and financial penalties, and the risk to workers and company reputation of unsafe working conditions can all impair loans.

“Put simply, if a business does not have a good sustainable profile it is a higher credit risk,” says Decoeur. MV Credit may be satisfied with a company’s fundamentals, the credentials of a company’s management, the structure of the deal and the valuation, but will not commit capital because key commercial practices are not sustainable.

And while MV Credit is attracted to the financial risk-return profile of the healthcare sector, it doesn’t invest in care homes, for instance. It believes that businesses that have a critical role in economy and society should not be subject to the profit motive.

Conclusion: surviving market stress

Leveraged loans are, historically speaking a high-performing asset class. But in times of high market stress only the most robust strategies will continue to deliver market-beating returns. More resilient strategies focus on less-cyclical businesses and use experience and knowhow to work with partners to avoid significant loan impairment.

“We have been in this market, and only this market, for 20 years,” notes Decoeur. “We have employed the same investment strategy that whole time. The only difference between now and then is we have a lot more experience.”

Published in May 2020

MV Credit Partners LLP

Registered Number : OC397214

Authorised and Regulated by the Financial Conduct Authority (FCA) with the FCA register number 67717.

45 Old Bond Street

London W1S 4QT

www.mvcredit.com

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2020 Natixis Investment Managers S.A. – All rights reserved

Integrating ESG Risks in Private Debt

Integrating ESG Risks in Private Debt

Private Debt Investing, With a Twist

Private Debt Investing, With a Twist

The Decline of the Distressed Debt Investor?

The Decline of the Distressed Debt Investor?