Rethinking the EM Corporate Bond Asset Class: Insights for Insurers

|

|---|

Consider that despite a strong US dollar, tight global liquidity and some commodity weakness in 2023, many core emerging markets demonstrated resilience and the markets took notice, resulting in solid returns. I see this as evidence of traction on reforms, the development of internal demand, and greatly improved central bank credibility. It is also likely a recognition of the diversification of the asset class that has come with its growth.

Looking into 2024, we believe the market’s expectation of a global easing in liquidity could be an incremental tailwind to EM debt’s 2023 resilience – over and above the persistent spread premium we see in EM corporate debt.

To what do you attribute the growth in the EM corporate debt opportunity set?

We have observed that industrialization, urbanization and an expanding middle class have fueled EM growth over the years. This economic transformation has expanded the investment universe as sector growth and industry consolidation led to companies with the scale, track record, and growth financing needs to attract the international bond market. In addition to regional and niche players, emerging markets are home to many strong global enterprises, some of which are world leaders in their respective industries. We note that the result has been more investment choices for a broader group of investors.

Historically, crossover investors from developed markets (DM) would dip in and out of the EM corporate asset class based on their view of beta and portfolio risk positioning. Or, they sought a spread pickup relative to sovereigns. We see much less of that behavior now. Instead, investors appear to be looking specifically at EM companies for their potential upside and the roles they can play in a portfolio. Beyond portfolio managers, we have found that the end investor has really evolved. For example, we are engaging with insurance companies, pension funds and large industrials discussing the EM credit asset class and how it can offer high-quality carry.

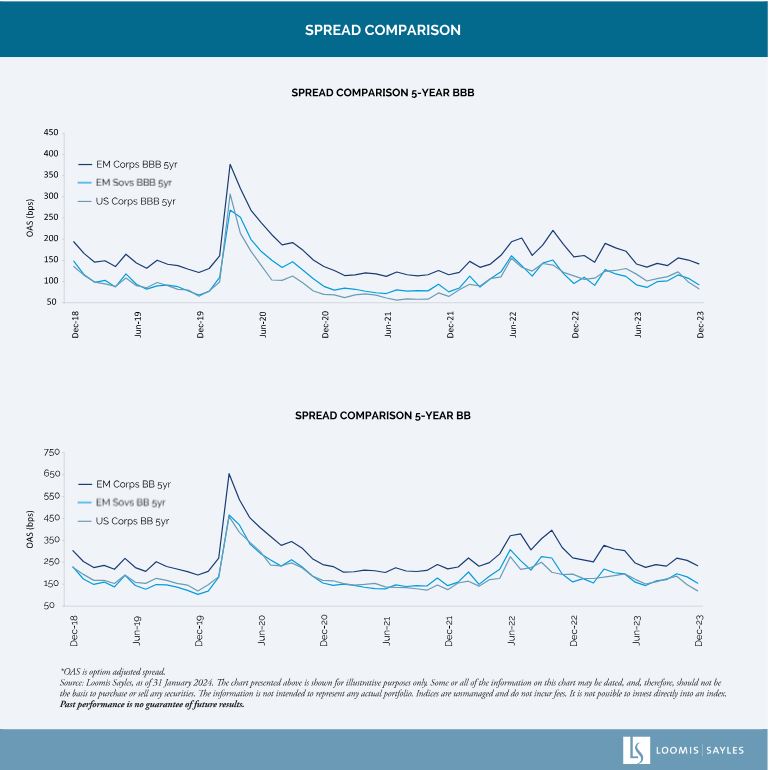

The EM corporate debt asset class has traditionally been compared to US high yield (HY) in terms of risk. Is this a fair comparison?

We believe that the low-quality image of the asset class is outdated based on several factors. The EM corporate opportunity set is, on average, investment grade and more than 70% of issuers are in Investment-grade-rated countries.1 In fact, debt metrics for EM companies are, on average, superior to what we see for developed market issuers. Also, it is important to remember that the credit rating for an EM company is often limited by the rating on the country where it resides. Often we find that even the companies rated high yield in EM can have stronger-than-expected credit metrics.

Given the changes you mentioned, does China still represent the key to EM performance?

In my view, China is not the driver of EM growth that it once was. EM countries continue to develop their own growth engines. These advances have contributed to some of the economic resilience we have witnessed.

That said, China is a large global trading partner and its health does have some implications for EM countries. At this juncture, we think its export levels have bottomed, and a rebound could be a tailwind for China growth, EM growth and global growth in 2024. We will be watching for exports to become less of a drag for China growth stabilization. We believe that China’s growth will be close to potential and likely be around 4.5% for 2024, but growth unevenness could persist. Conversely, we believe that China’s GDP could surprise to the upside if authorities stimulate more broadly than what has been done so far.

A subsidiary of Natixis Investment Managers

Investment adviser registered with the U.S. Securities and Exchange Commission (IARD No. 105377)

One Financial Center,

Boston, MA 02111, USA

www.loomissayles.com

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2024 Natixis Investment Managers S.A. – All rights reserved

An LDI Playbook for 2024

An LDI Playbook for 2024

Investment Outlook: Loomis Sayles

Investment Outlook: Loomis Sayles

Obligations : comment générer de « l'alpha prudent » ?

Obligations : comment générer de « l'alpha prudent » ?

Loomis Sayles - Investment Outlook - April 2024

Loomis Sayles - Investment Outlook - April 2024