Solving the Insurance Equation

Insurers need innovative investment strategies in response to regulation and low yields

Key Takeaways:

- The historic low yields as a result of Quantitative Easing are impacting insurers’ balance sheets and ability to meet liabilities. The challenge is compounded by regulation, such as Solvency II, which impedes investment solutions.

- Insurers require a new approach to investing, using innovative and tailored solutions. These solutions must be underpinned by appropriate reports, to comply with the complex web of reporting rules under new regulations.

- We outline solutions that can help insurers meet their goals - duration gap/non-traditional fixed income solutions, yield-enhancer solutions and volatility management solutions - and we expose the client benefits of insurance-specific tailor-made solutions

Resources

They are increasingly turning to the asset management industry, seeking a tailored approach to the specific challenges that the insurance industry faces. They need asset managers to provide analytical insight and strategic solutions on how to maximise returns. And they need asset managers to develop products that minimise capital requirements and, at the same time, produce appropriate reports in a timely manner to meet the new regulatory requirements.

QE and regulatory pressures

Quantitative Easing (QE) has shaped the world economy and the investment landscape since the global financial crisis. Since its introduction by the Federal Reserve in November 2008, assets held on the major central bank balance sheets have nearly trebled1. The impact of this is well known: long-term yields from core European sovereign debt are barely in positive territory, while spreads on many credit instruments have narrowed to levels that arguably do not compensate for the risk taken.

Moreover, QE is unlikely to be unwound any time soon: the Brexit vote has added further uncertainty to the world economic outlook that was already shaky amid concerns about the outcome of the US presidential election approaches, perceived fragility in the Chinese economy and ongoing weakness in commodities prices.

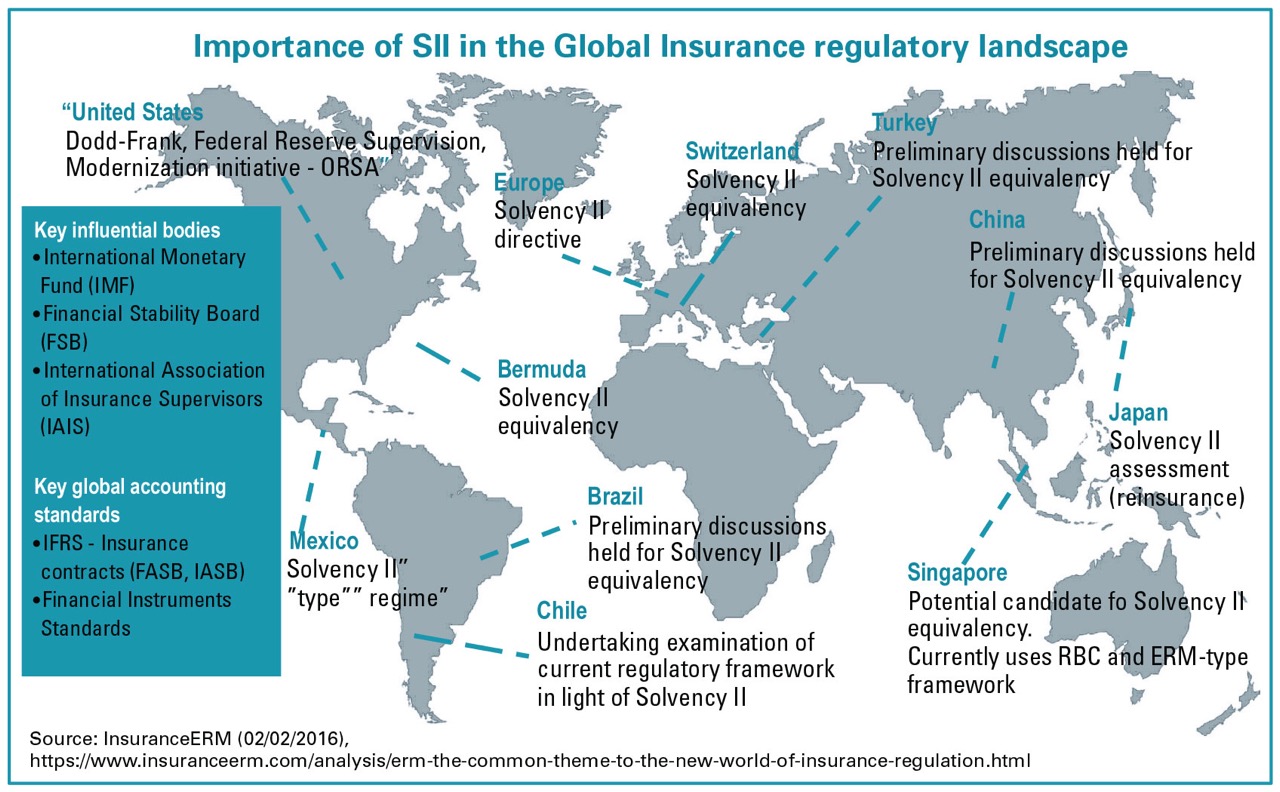

The effects of QE are borne by all investors, but the impact on insurers is compounded by huge regulatory changes to the industry. Led by the EU’s Solvency II Directive (SII), regulators around the globe are imposing capital constraints on insurers. SII has “brothers and sisters” around the world. Japan, Bermuda and Switzerland have already implemented an equivalent regime and many others, such as Australia, Hong Kong, Singapore, South Korea, Mexico, Chile and South Africa, are likely to adopt regimes which have many similarities with SII. In addition, the EU-US Insurance Project aims to align consumer protection and effective supervision between the two blocs.

The challenge for insurers

When SII was conceived back in 2002, few investment teams at the major insurers predicted the dramatic and prolonged drop in interest rates and the compression in spreads. The simultaneous combination of implementation deadlines for SII and historically low bonds yields has created a perfect storm for insurers. For those based in countries where life products have guaranteed high returns relative to yields on sovereign debt, the question of how to continue meeting these guarantees is being asked in boardrooms and among shareholders. These insurers cannot pass on low interest rates to policyholders, and the duration gap between their assets and liabilities can be very high. These insurers are in great need of effective, non-traditional fixed income solutions.

Even in those European countries, as well as in the US, where guaranteed products are less common or where insurers have been able to pass on low rates to policyholders, the capital surplus will be endangered if low rates persist. These insurers need to allocate more to yield-enhancer assets in order to strengthen the balance sheet over the longer term.

In the past, insurers managing guaranteed products were able to populate their portfolios with a mix of government and investment grade corporate bonds, and a smaller allocation to equities. Equally, insurers without such immediate cashflow obligations and with a longer-term outlook, could have invested heavily in equities. either of these options is now viable due to the dual effects of QE and SII (and its siblings).

While QE has essentially created the problem, SII puts obstacles in the way of many of the possible solutions. A decade ago, volatility and risk management were not explicitly managed by many investors; today, SII has made them priority items on the agenda of insurers’ investment committees. No discount rate and no asset-liability modelling can be applied without explicit reference to regulatory edicts such as the Solvency Capital Requirement (SCR) under SII.

In short, insurers require a new approach to investing, using innovative and tailored solutions and products. These innovative solutions need to be underpinned by appropriate reports, to comply with the complex web of reporting rules that SII imposes.

Innovative investments

Given the disparity of assets, liabilities and investment resources found at individual insurers, and the variation in their products and underlying client types, investment returns and cashflows needs will be highly dispersed. Asset managers will need to engage insurers to uncover their true needs, and then apply tailor-made solutions. A collaborative approach to finding solutions will depend on asset managers being able to develop the appropriate infrastructure that allows them to assess insurers’ key issues and apply a thoughtful, relevant approach to them.

The common factors in this approach will be a focus on risk, efficiency, capital charges, accounting, and for some, liquidity. Many investors, seeking to optimise the portfolio’s risk-return profile and the cost of capital, will diversify their investments beyond the traditional asset classes, into alternatives, real and unlisted assets.

Natixis Global Asset Management has developed three principal solutions that are applicable to insurers around the world and delivered mainly through open-ended funds:

- Duration gap/non-traditional fixed income solutions.

These include global bonds, short duration bonds, high yield, emerging market bonds, bank loans, corporate private debt and real assets debt. - Yield-enhancer solutions.

These include global equity, US equity, sustainable equity, private equity, real estate equity, infrastructure equity and total return funds. - Volatility management solutions.

These include minimum variance, overlay capabilities, volatility equity and equity capital optimization strategies.

It is possible to allocate to equity while reducing inherent equity risk, thereby staying within SCR limits. Natixis offers solutions in this area:

One solution is to use overlay strategies aimed at covering equity beta, and reducing equity volatility and the equity SCR. This could be implemented separately or in combination depending on the needs of the insurer.

Another solution is to combine a low volatility equity strategy with protected active management linked to an explicit bank guarantee. The objective is to achieve a return similar to that of direct equity market exposure, while reducing volatility by around 30% over the market cycle. The explicit bank guarantee ensures capital protection, which leads to a reduced SCR over three years.

Scaling up reporting

Investment solutions must take into account much more than the simple likelihood of outperformance of an asset or a product when creating a portfolio. In addition to taking into account risk, efficiency, accounting, capital charge and liquidity, there is a critical need for transparent portfolios and comprehensive reporting in accordance with the Solvency II Directive and similar regulation.

Natixis Global Asset Management’s dedicated relationship and reporting unit

Natixis has developed a specialized business relationship line with insurance companies and mutual insurers, offering:

- An experienced sales team fully dedicated to insurance.

- Services specific to insurers such as SCR calculation (standard formula), QRT (Quantitative Reporting Templates) and TPT (Tripartite Template) reporting, and transparent inventories

- Regulatory watch

- Risk monitoring at three levels of insurance management: the investment teams and risk departments of each of Natixis affiliates, and at the holding level.

It’s a specialised job

We think insurance investing has become a specialist activity that only a few asset managers have the capabilities to tackle successfully.

Asset managers need to have long experience of serving insurers to be successful in the new post-QE, SII era. Natixis Global Asset Management has over 30 years of experience in servicing insurance assets, managing over €250bn for 120 insurance clients in 14 different countries, and has helped its insurance clients to invest in 75 different asset classes via its broad range of open-ended funds and tailor-made solutions.

Natixis Global Asset Management has developed a long-term and trust-based relationship with insurers by offering highly experienced insurance management expertise through dedicated mandates, whatever the need: these include matching portfolios, diversification under liquidity constraints, active management under SCR constraints and investment management focusing on the accounting impact and a yield optimization target. Natixis insurance solutions have demonstrated a strong, consistent and stable return rate over time, whatever the market conditions.

The group also offers insurers independent and bespoke portfolio analysis with a focus on risk management (correlations matrix, value at risk, asset allocation building blocks, risk budgeting, factor analysis, stress test, peer group analysis). Understanding risk exposures helps to improve diversification, which can help to reduce the overall risk profile. This risk-minded investing approach seeks to achieve better returns with lower overall volatility in order to build more durable portfolios.

Moreover, Natixis Global Asset Management’s insurance clients benefit from a dedicated and specialized business relationship, as well as reporting and services specific to insurance management.

Published in November 2016.

Natixis Global Asset Management S.A.

RCS Paris 453 952 681

Share Capital: €156 344 050

21 quai d’Austerlitz, 75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2016 NATIXIS GLOBAL ASSET MANAGEMENT S.A. – All rights reserved

Insurance survey

Insurance survey

Loomis Sayles - Investment Outlook - April 2024

Loomis Sayles - Investment Outlook - April 2024

Natixis IM Solutions - Market Review - March 2024

Natixis IM Solutions - Market Review - March 2024

2024, A Singular Context of Volatility in the Markets?

2024, A Singular Context of Volatility in the Markets?