Inflation Protection: An Equity-Centric View

While the world waits and hopes for many of the supply chain related inflationary pressures to subside, the speed and pace of inflation normalization feels highly uncertain. How can an investor enhance returns during time periods when inflation exceeds market expectations?

Reducing fixed income duration, investing in TIPS (Treasury Inflation Protected Securities), or adding commodity futures are a few timeless portfolio construction ideas that can help provide more durable returns in inflationary environments -- but perhaps at a cost of sacrificing returns if inflation falls flat. So we present a slightly different approach: an equity-centric view of inflation protection that can better position portfolios for the current environment.

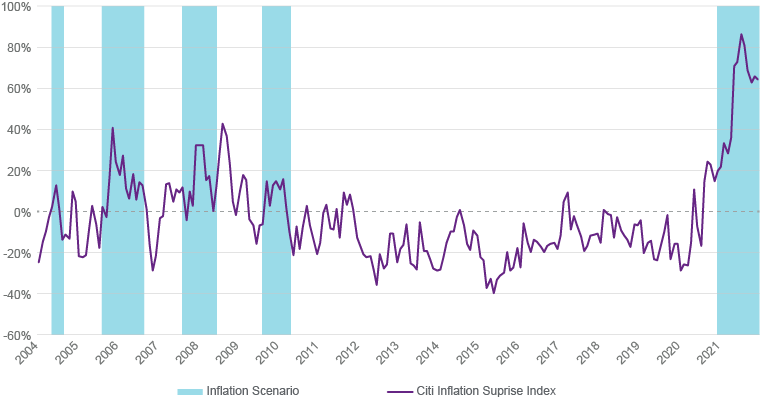

There’s no need to go back to the 1970s for historical perspective on performance during unexpectedly high inflation. Looking at the Citigroup Inflation Surprise Index, we isolated five more recent time periods where inflation came in hot (Figure 1).

Figure 1 - When Inflation Came In Hot...

Source: Bloomberg; Natixis Investment Managers Solutions as of 12/31/2021

Some Industries Fared Better Than Others

Which industries tended to outperform on a risk-adjusted basis during these five regimes? Equity REITs (Real Estate Investment Trusts), Metals & Mining, Oil & Gas, and Banks, to name a few. Which tended to underperform? Semiconductors, Wireless Telecom, and Auto Components were three that consistently lagged the broad market during these time periods.

Using this historical performance data, we developed a scoring system that can be applied to any equity product. Products with high allocations to industries with strong performance and low allocations to industries with weak performance during these high inflation periods will score well. These product scores can then be rolled up to the portfolio level to evaluate your overall inflation protection.

Key Takeaways

We applied this framework across the full Morningstar equity universe. This exercise highlighted a number of factors to consider when building inflation protection:

- Value/growth allocation matters. All else equal, value strategies tend to outperform in inflationary surprises. Favoring a value tilt or avoiding a meaningful growth tilt can enhance inflation protection.

- US/Non-US allocation matters less than you might think. While international equities offer more inflation protection than US equities, in our view it’s not enough to move the needle in a meaningful way.

- Small allocations to select asset classes can provide significant inflation protection at the portfolio level. Natural resources, infrastructure, real estate, and energy-focused products should be some areas to target when building inflation protection.

- Manager selection is important as well. If you use multiple managers in your larger category allocations – large cap value, for example – make sure your managers are complementary from an inflation perspective.

If you’re interested in applying this framework to the portfolios you manage, please download the slide deck, and don’t hesitate to contact your Natixis representative.

This content contains “forward-looking statements” concerning activities, events or developments that the Portfolio Analysis and Consulting (PAC) group expects or believes may occur in the future. These statements reflect assumptions and analyses made by PAC analysts based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond PAC’s control, they are not guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements.

Equity securities are volatile and can decline significantly in response to broad market and economic conditions.

Real estate investing may be subject to risks including but not limited to declines in the value of real estate, risks related to general economic conditions, changes in the value of the underlying property owned by the trust, and defaults by borrowers.

Commodity-related investments, including derivatives, may be affected by a number of factors including commodity prices, world events, import controls, and economic conditions and therefore may involve substantial risk of loss.

Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis”) and does not sponsor, endorse or participate in the provision of any Natixis services, funds or other financial products. Index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

4655484.1.1

Direct Indexing: Checking the Box

Direct Indexing: Checking the Box

Tax Management Update – Q1 2024

Tax Management Update – Q1 2024