Is This a Good Time to Consider Corporate Bonds?

But wouldn’t rising spreads sink corporate bonds, particularly considering our prospects for a recession? Data from the past four recessions provide some context.

Key Takeaways:

- Investment grade corporate yields touched 5% in mid-June, their highest levels since 2009.

- Spreads have historically increased in recessionary periods.

- But economic data remains strong, making it unlikely that a recession is imminent.

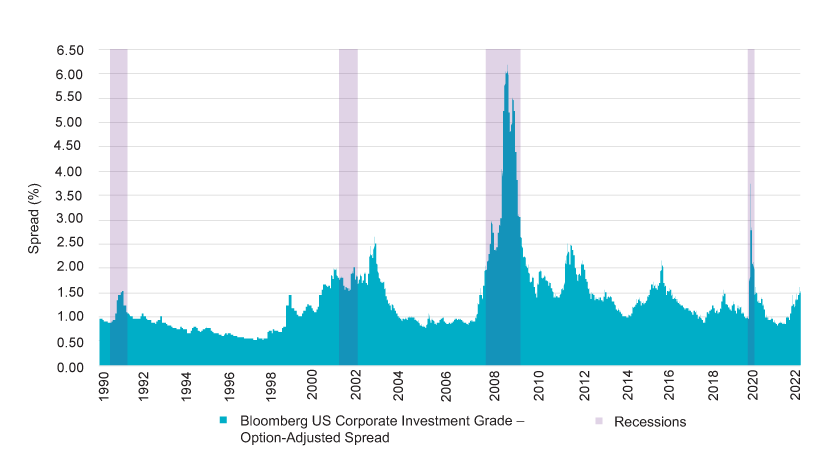

Figure 1 – Spreads Have Historically Peaked During Recessions – Investment grade corporates option-adjusted spread (1/1/90–6/30/22)

Source: FactSet, Bloomberg, Natixis Investment Managers Solutions

The four most recent US recessions include two milder recessions (July 1990 – Mar 1991; Mar 2001 – Nov 2001), one major recession (Dec 2007 – June 2009), and one major but short-lived recession (Feb 2020 – April 2020). All four are characterized by elevated spread levels. Three out of four are characterized by multi-year peaks in spreads that began to abate before the recession ended. Peak spreads – whether in the middle of a recession or not – are the ideal time to buy corporate bonds, as spread compression provides an additional kick to overall returns.

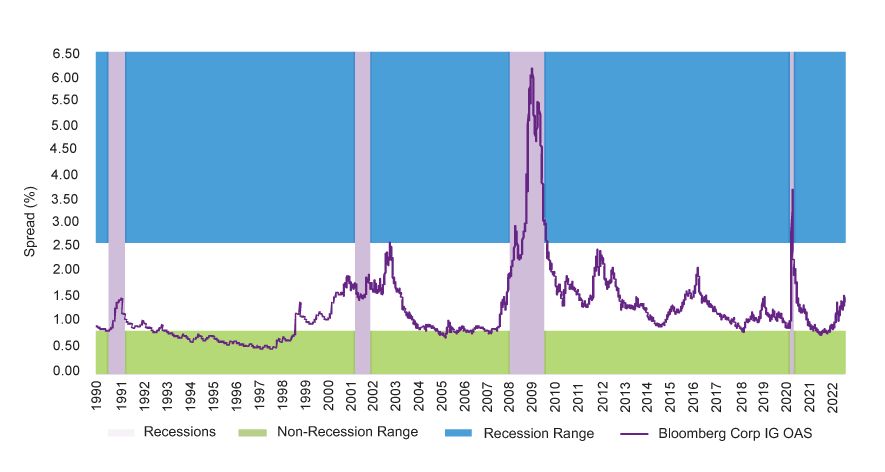

Credit Spreads as a Recession Signal

Since 1990, the non-recessionary average option-adjusted spread (OAS) is 117 basis points, while the recessionary average is 256 bps. Looking at those figures, the recent high-water mark of 160 bps OAS on 7/5/22 feels tame. But this average recession figure is biased upward by the extreme values experienced in the depths of the Great Financial Crisis. So another way to think about the signaling capabilities of spreads is shown in the “recession zones” in Figure 2.

Figure 2 – Spreads and Recession Zones (1/1/90–6/30/22)

Source: FactSet, Bloomberg, Natixis Investment Managers Solutions

Looking back at the two milder recessions, we have already surpassed the peak spreads of 1990–91, and are 40 bps shy of peak spreads experienced during 2001–02. In other words, corporate bonds are arguably priced as if we are in or close to a mild recession right now. And consider that despite the equity market losses, inverted yield curve, inflation surprises, you name it… there is a breadth of strong economic data making it incredibly unlikely that we are in a recession or that a recession is imminent:

- Unemployment remains low.

- Household and corporate balance sheets remain strong.

- Credit card transactional data shows consumers are still consuming.

Good Time for Investment Grade Corporates?

If your base case is that we’re in the early innings of a GFC-style recession, then by all means stay away from IG corporates. But if you think we’ve got some runway ahead before perhaps a milder recession (or if you think we’re already in a recession), then most of the pain has already occurred and the future prospects are attractive. We have the highest yields since 2009 and the potential for additional price appreciation if rate volatility subsides and/or corporate earnings prove more resilient than expected. As well as some cushion for downside protection, thanks to the elevated yields.

The perfect entry point is impossible to predict, and some investors may want to lean into corporate bonds over multiple steps as an additional risk management lever. But adding to corporate bonds, perhaps funded from Treasuries, mortgages, or cash, looks like a return-enhancing trade for many portfolios that sorely need one.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

All investing involves risk, including the risk of loss. Investment risk exists with equity, fixed income, and alternative investments. There is no assurance that any investment will meet its performance objectives or that losses will be avoided. Investors should fully understand the risks associated with any investment prior to investing.

4863922.1.1

Portfolio Construction Fundamentals

Portfolio Construction Fundamentals