Positioning Portfolios for Fading Inflation

Authors’ Note: This article is part two in a two-part series on positioning equity portfolios with an eye toward inflation-sensitivity. Our original article, Inflation Protection: An Equity-Centric View, focused on enhancing returns in periods of surprise high inflation. Here we offer suggestions for positioning portfolios for declining inflation.

Earlier in 2022, supply-chain-related inflationary pressures dominated headlines, and we suggested that the pace of normalization was uncertain. This led us to develop a framework to evaluate the inflation-sensitivity of equity portfolios. The idea was two-fold: First, investors with no view on the inflation outlook could diversify their portfolios by allocating to strategies positioned to outperform in rising inflation environments as well as strategies positioned to benefit from declining inflation environments. Our research suggested that many investors unknowingly have portfolio tilts toward one or the other, particularly when recent performance influences manager selection decisions. Second, for investors looking to make a tactical tilt, adding inflation protection to a portfolio would help position for outperformance in the event that inflation accelerated and remained persistently high for the next several months.

Has Inflation Peaked?

As we begin to see year-over-year inflation showing signs of peaking, our focus is shifting toward positioning to benefit from disinflation. While we haven’t seen clear and convincing evidence that inflation is rolling over in the commonly followed CPI (Consumer Price Index), there are some recent developments that lead us to believe that inflation is set to decelerate in the months and quarters ahead: falling/stabilizing commodity prices, falling shipping costs, normalizing supply chain constraints, goods inventory gluts, a stronger US dollar, and fading pandemic effects.

So what portfolio shifts can you make to reposition for this environment? Lengthening duration, shifting from TIPS (Treasury Inflation-Protected Securities) to nominal Treasuries, and reducing commodities exposure are traditional ways to lighten up in your portfolio inflation hedges. But we’d like to highlight an alternative approach that focuses on repositioning an equity sleeve.

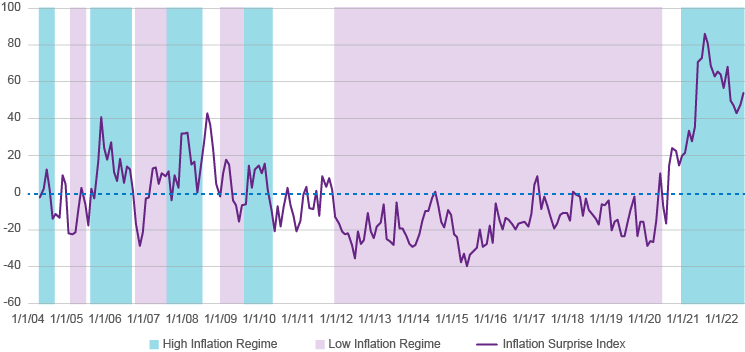

As noted previously, there’s no need to go back to the 1970s for historical perspective on equity performance during periods of unexpected inflation. Looking at the Citigroup Inflation Surprise Index, we isolated recent time periods characterized by unexpectedly high and low inflation prints (Figure 1).

Risk-adjusted performance in these high inflation regimes showed clear differentiation at the industry level. Equity REITs (Real Estate Investment Trusts), Metals & Mining, and Oil & Gas were a few notable industries that outperformed, while industries like Semiconductors, Wireless Telecom, Autos, and Airlines typically underperformed. It stands to reason that as inflation-related headwinds fade, these historical underperformers will have an opportunity to lead a rebound in equity markets. Using this historical performance data, we developed a scoring system that can be applied to any equity product. Products with high allocations to inflation-protection industries and/or low allocations to inflation-fading industries receive more positive scores, while products with high allocations to inflation-fading industries and/or low allocations to inflation-protection industries receive more negative scores. These product scores can then be rolled up to the portfolio level to evaluate overall inflation sensitivity.

Key Takeaways

We applied this framework across the full Morningstar equity universe. This exercise highlighted a number of things to keep in mind as you potentially reposition your portfolio for slowing inflation.

This content is provided for informational purposes only and should not be construed as investment advice. References to specific securities or industries should not be considered a recommendation. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Natixis Investment Managers Solutions, or any Natixis Investment Managers affiliates. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

This content contains “forward-looking statements” concerning activities, events or developments that the Portfolio Analysis and Consulting (PAC) group expects or believes may occur in the future. These statements reflect assumptions and analyses made by PAC analysts based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond PAC’s control, they are not guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements.

Equity securities are volatile and can decline significantly in response to broad market and economic conditions.

Real estate investing may be subject to risks including but not limited to declines in the value of real estate, risks related to general economic conditions, changes in the value of the underlying property owned by the trust, and defaults by borrowers.

Commodity-related investments, including derivatives, may be affected by a number of factors including commodity prices, world events, import controls, and economic conditions and therefore may involve substantial risk of loss.

Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis”) and does not sponsor, endorse or participate in the provision of any Natixis services, funds or other financial products. Index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

Earlier in 2022, supply-chain-related inflationary pressures dominated headlines, and we suggested that the pace of normalization was uncertain. This led us to develop a framework to evaluate the inflation-sensitivity of equity portfolios. The idea was two-fold: First, investors with no view on the inflation outlook could diversify their portfolios by allocating to strategies positioned to outperform in rising inflation environments as well as strategies positioned to benefit from declining inflation environments. Our research suggested that many investors unknowingly have portfolio tilts toward one or the other, particularly when recent performance influences manager selection decisions. Second, for investors looking to make a tactical tilt, adding inflation protection to a portfolio would help position for outperformance in the event that inflation accelerated and remained persistently high for the next several months.

Has Inflation Peaked?

As we begin to see year-over-year inflation showing signs of peaking, our focus is shifting toward positioning to benefit from disinflation. While we haven’t seen clear and convincing evidence that inflation is rolling over in the commonly followed CPI (Consumer Price Index), there are some recent developments that lead us to believe that inflation is set to decelerate in the months and quarters ahead: falling/stabilizing commodity prices, falling shipping costs, normalizing supply chain constraints, goods inventory gluts, a stronger US dollar, and fading pandemic effects.

So what portfolio shifts can you make to reposition for this environment? Lengthening duration, shifting from TIPS (Treasury Inflation-Protected Securities) to nominal Treasuries, and reducing commodities exposure are traditional ways to lighten up in your portfolio inflation hedges. But we’d like to highlight an alternative approach that focuses on repositioning an equity sleeve.

As noted previously, there’s no need to go back to the 1970s for historical perspective on equity performance during periods of unexpected inflation. Looking at the Citigroup Inflation Surprise Index, we isolated recent time periods characterized by unexpectedly high and low inflation prints (Figure 1).

Figure 1 – Inflation Environments Since 2004

Source: Citigroup; Natixis Investment Managers Solutions

Risk-adjusted performance in these high inflation regimes showed clear differentiation at the industry level. Equity REITs (Real Estate Investment Trusts), Metals & Mining, and Oil & Gas were a few notable industries that outperformed, while industries like Semiconductors, Wireless Telecom, Autos, and Airlines typically underperformed. It stands to reason that as inflation-related headwinds fade, these historical underperformers will have an opportunity to lead a rebound in equity markets. Using this historical performance data, we developed a scoring system that can be applied to any equity product. Products with high allocations to inflation-protection industries and/or low allocations to inflation-fading industries receive more positive scores, while products with high allocations to inflation-fading industries and/or low allocations to inflation-protection industries receive more negative scores. These product scores can then be rolled up to the portfolio level to evaluate overall inflation sensitivity.

Key Takeaways

We applied this framework across the full Morningstar equity universe. This exercise highlighted a number of things to keep in mind as you potentially reposition your portfolio for slowing inflation.

- Value/growth allocation matters. Growth strategies have historically faced pressure from higher inflation and tighter financial conditions. Shifting some of your value to growth can help capture meaningful upside as these headwinds fade.

- Small allocations to sector-specific products can move the needle at the portfolio level. Technology, communication services, and consumer discretionary-focused products have the highest allocations to industries that have historically struggled during high inflation periods.

- US/Non-US allocation matters less than you might think. International strategies score as having better inflation protection than US strategies, but it’s not meaningful enough to warrant a major shift. Currency exposure can also play a role in the return outcome. For example, a stronger dollar can offset any return advantage from the inflation-related tilt. Ultimately, there is a wide range of inflation-sensitive and inflation-fading strategies in both US and non-US markets, so making inflation-related tilts becomes more of a manager selection exercise.

- Manager selection is important. Performance dispersion across Morningstar categories has been significant in 2022. It’s a good exercise to take a close look at drivers of recent performance and determine if now is the time to lighten up on products that have benefited (relatively speaking) from chunky allocations to inflation beneficiaries and lean into products that have more industry diversification.

This content contains “forward-looking statements” concerning activities, events or developments that the Portfolio Analysis and Consulting (PAC) group expects or believes may occur in the future. These statements reflect assumptions and analyses made by PAC analysts based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond PAC’s control, they are not guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements.

Equity securities are volatile and can decline significantly in response to broad market and economic conditions.

Real estate investing may be subject to risks including but not limited to declines in the value of real estate, risks related to general economic conditions, changes in the value of the underlying property owned by the trust, and defaults by borrowers.

Commodity-related investments, including derivatives, may be affected by a number of factors including commodity prices, world events, import controls, and economic conditions and therefore may involve substantial risk of loss.

Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis”) and does not sponsor, endorse or participate in the provision of any Natixis services, funds or other financial products. Index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

4970703.1.1

Portfolio Construction Fundamentals

Portfolio Construction Fundamentals