Traditional Diversification Is Working Again

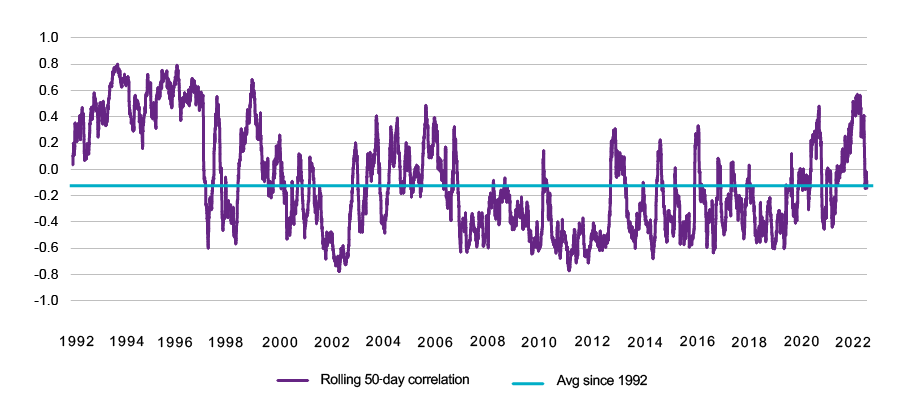

Don’t look now, but stock-bond correlations finally peaked in early December and have been plummeting ever since. The trailing 50-day correlation between the S&P 500® and the Bloomberg US Aggregate Bond Index (the Agg) is now modestly negative for the first time in about a year (Figure 1). Traditional diversification is working again.

Figure 1 – Correlation between S&P 500® and Bloomberg US Aggregate Bond Index (1992–2022)

Source: Bloomberg

In the two weeks following the collapse of Silicon Valley Bank in March, the S&P 500® lost more than 1% on four separate days. But all four days saw meaningfully positive return from the Bloomberg US Aggregate (Figure 2).Figure 2 – Stock returns down, bond returns up in March

| Date | S&P 500® Return | Bloomberg US Agg Return |

|---|---|---|

| 3/9/23 | -1.8% | +0.4% |

| 3/10/23 | -1.4% | +1.2% |

| 3/17/23 | -1.1% | +0.8% |

| 3/22/23 | -1.6% | +1.0% |

Source: Bloomberg

Why Is This Finally Happening Now? And What Took So Long??Risk-off sentiment typically leads to lower levels of the expected future path of cash, lower term premium, or both. This leads to lower bond yields and higher bond prices. But this relationship breaks down if the risk-off sentiment has been driven by unexpectedly higher inflation as we saw recently. A similar dynamic played out post-World War II in the late 1940s, the Vietnam War / Great Society backdrop of the late 1960s, and of course in 2022.

In these cases, rates weren’t moving because the growth outlook was being repriced. Rates were moving because the inflation outlook was being repriced. With each subsequent hot inflation print last year, the market realized the Fed would need to raise rates more aggressively than initially expected. And with more rate hikes anticipated, stocks and bonds both sold off. In November, as inflation started to show signs of cooling, an easing of some of these fears led to the reversal of some of these return patterns. Stocks and bonds both rallied. Great for investors, but it meant the correlations between stocks and bonds remained elevated. Bonds were still not technically providing much diversification.

Shifting Expectations

But now we are increasingly seeing an environment where fixed income yields move because of shifts in the Federal Reserve’s expectations due to changes in the growth outlook. For example, the market prices in cuts assuming recession odds are increasing. And no longer because of shifts in Fed expectations due to inflation. We’re having more “stocks up and bonds down” days as well as “stocks down and bonds up” days. In other words, lower stock-bond correlations. Diversification is working again.

Time for High Quality Duration

So how can investors benefit from this? By having high quality duration in your portfolio. When stocks fall and bonds rally, it’s not the short-duration CDs, T-Bills, and money market funds that do well. It’s longer duration assets that benefit – like government bonds, corporate bonds, core strategies and core plus strategies. Many investors are comfortable hanging out in cash because of the attractive yields and the inverted yield curve. But you need to stay invested in a money market fund for a full year to achieve the headline yield. A six-month CD yielding 5% on an annualized basis is really only going to return 2.5% after six months and leave you with another decision to make after that. With correlations returning to more normal levels, we believe investors could be leaving money on the table in the scenario where equities decline over the next several months. Putting at least a portion of that money to work into high quality duration is a good risk management exercise.

The long and the short of it? Unlike a year ago, most investors are now comfortable with the notion of fixed income as an attractive total return resource for the long run. This year’s lower stock-bond correlations make fixed income an effective diversifier once again, as well.

This material is provided for informational purposes only and should not be construed as investment advice. The views and opinions contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Natixis Investment Managers, or any of its affiliates. The views and opinions are as of April 17, 2023 and may change based on market and other conditions. There can be no assurance that developments will transpire as forecasted, and actual results may vary.

All investing involves risk, including the risk of loss. Investment risk exists with equity, fixed income, and alternative investments. There is no assurance that any investment will meet its performance objectives or that losses will be avoided. Investors should fully understand the risks associated with any investment prior to investing.

This material may not be redistributed, published, or reproduced, in whole or in part. Although Natixis Investment Managers believes the information provided in this material to be reliable, including that from third party sources, it does not guarantee the accuracy, adequacy or completeness of such information.

This document may contain references to copyrights, indexes and trademarks that may not be registered in all jurisdictions. Third party registrations are the property of their respective owners and are not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis”). Such third-party owners do not sponsor, endorse or participate in the provision of any Natixis services, funds or other financial products.

Provided by Natixis Distribution, LLC, 888 Boylston St., Boston, MA 02199. Natixis Investment Managers includes all of the investment management and distribution entities affiliated with Natixis Distribution, LLC and Natixis Investment Managers S.A. Natixis Advisors, LLC provides advisory services through its division Natixis Investment Managers Solutions. Advisory services are generally provided with the assistance of model portfolio providers, some of which are affiliates of Natixis Investment Managers, LLC.

5640075.1.1

60/40 Portfolio Simplicity

60/40 Portfolio Simplicity

3 Questions for Your Cash Management and Short-Term Investment Allocations

3 Questions for Your Cash Management and Short-Term Investment Allocations