2018 Outlook of Institutional Investors

Key Takeaways:

- Allocations to passive strategies decline for third consecutive year; 75% believe the current market environment favors active management

- Alternative assets overshadow bonds as investors shift to Europe & emerging markets; Technology, healthcare, aerospace and financial sectors seen as top outperformers

- 72% are surprised volatility has been so low for so long and 59% say it’s a major concern, but geopolitical risks and asset bubbles are institutional investors’ the top concerns

- A majority say the growth of passive investing artificially suppresses volatility (59%), distorts relative stock prices and risk-return trade-offs (57%), and increases systemic risks (63%)

To position their portfolios for the volatility they expect as central banks gradually remove the monetary life support system in place since the financial crisis, they are also increasing allocations to non-traditional assets, including private equity, private debt, infrastructure and real estate, as they seek alternatives to bonds and hunt for higher returns in a crowded market.

Natixis surveyed decision makers at 500 institutional investment firms who, in sum, manage more than $19 trillion in assets for retirees, governments, insurance companies and other institutions. The survey found 59% believe that volatility has been artificially suppressed by flows into passive investment strategies. More than half (57%) believe the increase in passive investing is distorting relative stock prices and creating systemic market risks (63%), of which 72% believe individual investors aren’t yet aware.

Navigating active markets

Active strategies are increasingly in favour among institutions, with 76% who now believe the current market environment is likely to be favourable for active portfolio management.

Comparing passive and active approaches directly, a 57% majority say active managers outperform passive in the long run. Three-quarters of institutions (75%) say active managers are better at accessing emerging market opportunities – and a similar proportion (74%) say active managers provide better exposure to non-correlated asset classes.

Bond bubbles vs. equity volatility

An overwhelming three-quarters of institutions (77%) believe a prolonged period of low interest rates has led to the creation of asset bubbles. Moreover, looking ahead, 62% of institutional investors see interest rate rises as the top portfolio concern for 2018 – a potential trigger for a correction in fixed income values.

The survey also found asset bubbles rival geopolitical events – a concern for 74% following recent events – and asset bubbles rank ahead of interest rate increases (61%) as the factor institutions believe will have the most negative impact on their investment performance in 2018.

Institutional investors believe the bond market is the traditional asset class most likely to be entering a bubble. With 42% of institutional investors now expecting a ‘bond market bubble’, this represents almost twice the proportion who expect a real estate bubble (23%) – and is even comparable to the 64% who see a bubble in Bitcoin.

A substantial proportion of institutional investors (30%) also observe a ‘bubble’ in equity markets. Yet renewed volatility (rather than a sustained correction) is set to be the main feature for equities in 2018: an overwhelming 78% of institutions expect an increase in equity volatility next year. Looking back on the absence of volatility this year, a majority of institutional investors (59%) believe this is unsustainable and is in fact a cause for serious concern.

The hunt for diversification

Institutional investors are placing greater faith in both equities and uncorrelated, alternative investments to help them ride out such market challenges:

- Equity exposures have risen to 37.1% (vs. 33.8% in 2016), while there has been a small decline in fixed income allocations, now 33.9% compared to 35.0% in 2016.

- Potentially reflecting fears of a bubble in fixed-income valuations, one third of institutional investors (33%) are decreasing the amount of high yield corporate debt they hold, while a quarter (26%) are doing the same with their holdings of government debt.

- Almost two-thirds (64%) say fixed income is no longer providing its traditional risk management role in portfolios, while 60% of institutions now believe traditional assets in general are too highly correlated to provide distinctive sources of return.

- By contrast 78% say increasing the use of alternatives is an effective way to manage risk – and almost the same proportion of institutions go further, believing alternative investments are in fact essential to diversify portfolio risk (70% vs. 67% a year ago).

- Within alternatives, there is also an appetite for illiquidity, as 74% believe potential returns make such investments worth the risk associated with fixed timeframes. Private equity is the most popular example with 39% of institutions increasing their private equity investments – and two-thirds (67%) are satisfied with the performance of private equity investments in their portfolio.

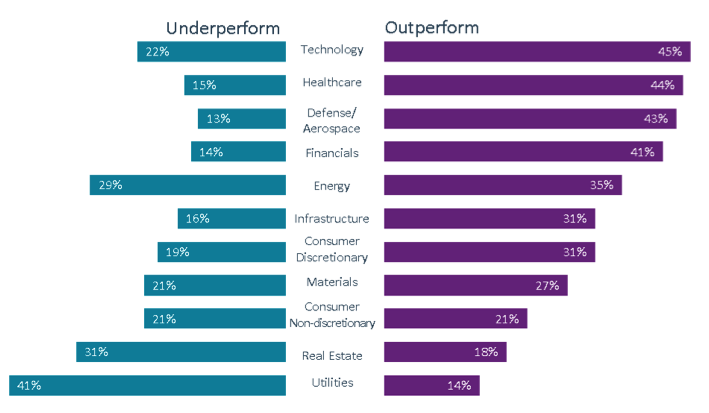

- In terms of sector picks: more institutions (45%) expect the technology sector to outperform the market in 2018 above any other sector, followed by healthcare (44%), defence/aerospace (43%) and financials (41%). Institutional Investors’ 2018 Sector Outlook

In direct competition to fixed income, more than three quarters of institutional investors now say that private debt provides higher risk-adjusted returns than fixed income vehicles (up from 73% a year ago) – and 36% of institutions are currently increasing their private debt holdings.

A longer-term view on the sustainability of returns is also emerging. Three-in-five (60%) institutions now say incorporating Environmental and Social Governance (ESG) practices will be standard for all managers within the next five years. This appears to be for practical purposes as much as moral; a similar majority (59%) say there is alpha to be found in ESG investing.

Methodology

Natixis surveyed 500 institutional investors including managers of corporate and public pension funds, foundations, endowments, insurance funds and sovereign wealth funds in North America, Latin America, the United Kingdom, Continental Europe, Asia and the Middle East. Data was gathered in September and October 2017 by the research firm CoreData. The findings are published in a new whitepaper, “It’s the end of the world as they know it. And they feel fine.” For more information, download our report Institutional Investor Outlook for 2018.

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

21 quai d’Austerlitz, 75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2017 Natixis Investment Managers. – All rights reserved

2015 Global Survey of Institutional Investors

2015 Global Survey of Institutional Investors

2016 Global Survey of Institutional Investors

2016 Global Survey of Institutional Investors

Mirova Monthly Market Review & Outlook - April 2024

Mirova Monthly Market Review & Outlook - April 2024

Russia-Ukraine: The Beginning of the End?

Russia-Ukraine: The Beginning of the End?