Local Bonds With Global Appeal

In a Q&A, Jim Grabovac, CFA and Steve Wlodarski, CFA of McDonnell Investment Management, explain how non-US investors could benefit from allocating to US municipal bonds.

Key Takeaways:

- The $3.83 trillion municipal market provides capital market access to US state and local governments, and to projects ranging from schools, hospitals, roads and airports, to water systems and power plants.

- Nearly 70% of the municipal market is rated AA or higher, compared with just 22% for the corporate market. And munis provide a modest yield pick-up versus corporate bonds and a significant yield uplift over Treasuries.

- For corporates and insurers, munis can be used to match liabilities and there is preferential treatment for munis under Solvency II. In the portfolios of very long-term investors such as pension funds, munis sit between Treasuries and corporate bonds, providing strong capital protection with yield uplift and diversification benefits.

Resources

A. The US Municipal Market is seeing increased interest from global investors. Long the domain of domestic buyers attracted by the exemption from federal tax, the municipal market began to draw the attention of non-US investors in 2009 with the onset of the Build America Bond Program (BAB), which resulted in a burst of issuance of subsidised taxable municipal bonds designed to help spur infrastructure investment in the wake of the economic downturn. Good quality and yield pickups versus US corporates attracted new buyers to the asset class and that participation has continued to grow.

Q. So what exactly are “munis”?

A. The municipal market provides capital market access to US state and local governments and their agencies. Issuance is broadly categorised as either General Obligation Debt, which is backed by a taxing authority, or Revenue Debt, which is backed by a specific stream of revenues such as tolls, fees and excise taxes. Within these broad categories are issuances for schools, hospitals, roads, airports, water systems, power plants and many other purposes. There is $3.8 trillion in US municipal debt outstanding1, which equates to somewhat less than half the size of the US corporate market and less than a third of the size of the US Treasury market. In comparison with sovereign debt markets, however, the municipal market would be the third largest issuer after the US and Japan. The municipal market is also highly diverse, with an estimated 50,000 issuers.2

Q. How risky are munis compared with corporate bonds?

A. Credit quality across the municipal market is generally high in comparison to the corporate market. Using Bloomberg Barclays indices data as a proxy, nearly 70% of the municipal market is rated AA or higher, compared with just 22% for the corporate market. Meanwhile, only 7% of munis are rated BBB, compared with 44% of corporate issuance.3 In addition to high average quality, the municipal market also has a much lower historical default rate as well as a higher recovery rate in the event of default.4 This is not meant to suggest that the municipal market is devoid of credit problems; underfunded pensions and other long-term liabilities represent a significant fiscal challenge for many issuers, particularly those that were over-leveraged heading into the credit crisis. But broadly speaking, the market has good fundamental credit quality, which has been bolstered by an eight-year economic recovery. There is some liquidity risk premium, as the market encompasses a large number of small issuers who come to market infrequently. Since the municipal market is dominated by higher rating categories compared to corporate bonds, we view liquidity risk as being low.

Q. How do you pick munis for your portfolio?

A. One of our strengths as a firm is having a research database which tracks about 6,500 individual municipal securities. In any given year, our analysts produce written reviews on over 500 names, which requires both deep credit research resources and cutting-edge credit technology. The analysts issue rating and momentum scores to each issue. The momentum score reflects if fundamentals are improving; we are typically looking to invest in issuers who are moving from a neutral or slightly negative momentum score to a positive score.

Q. How granular is your research?

A. The higher we perceive the risk, the more we research. Larger issuers release financials on a quarterly basis, but smaller issuers often require much greater scrutiny. For a hospital project, for example, we will look at whether financials are released on time; we examine the business model, the strategic plan, the business plan, its relative positioning in the market, its dependence on federal programs such as Medicare and Medicaid, and so on. We will follow up with conversations with CFOs if we think it’s necessary.

Q. What experience do you have managing municipal bond portfolios?

A. All our resources are focused on fixed Income; that’s our business. Two-thirds of the assets we manage are munis. In terms of skills and organisation, we’re different in that our portfolio managers and research analysts work as an integrated team, whereas in many firms, research is seen as an in-house ratings agency. We currently have 11 credit research analysts on staff, which is significant for our $11bn in AuM. These analysts, many of whom have 20 or more years of experience, allow our process to be research-driven across credits, markets and portfolios. They also serve as the core of our strong risk control culture and allow us to evaluate opportunities across the new issue market, which totalled $445B in 20161, the secondary market and the entire yield curve.

Q. What yields can investors expect?

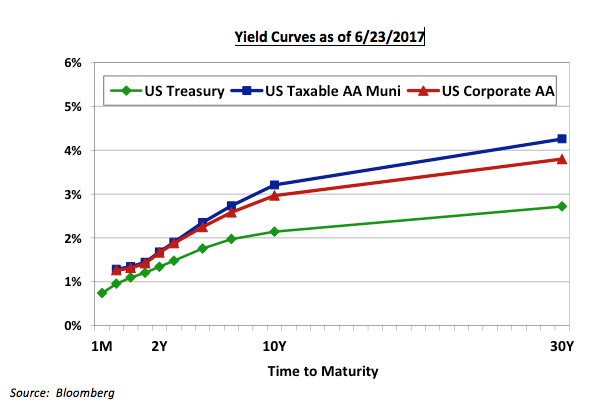

A. The municipal liquidity give-up tends to result in a modest yield pick-up versus comparably-rated corporate bonds and a significant yield uplift over Treasuries in the long-term, as the chart below shows.5 The level of return depends on the specific strategy. A boutique like McDonnell is uniquely positioned to exploit the trading inefficiencies of the market. We are large enough to have a significant market presence, but not so large as to limit our ability to be flexible and selective.

Q. How attractive are munis to non-US investors?

A. There is strong interest among US individuals because municipal interest income is usually exempt from federal taxes. But take-up by non-US investors in taxable issuance – which attracts higher yields - is increasing steadily. According to the Federal Reserve, non-US holders had accumulated $90.4B of munis (as of Q1-2017), or 2.3% of outstanding issuance.6 This represents an increase of 25% from the end of 2010.

Q. What kinds of investors should be interested in munis?

A. For corporations and, in particular, insurers, munis are increasingly used to match liabilities. In contrast to most segments of the fixed-income market, municipal issuance is typically comprised of a combination of serial and term bonds, with maturities staggered from one to 30 years. As a consequence, investors are afforded opportunities to invest in the 10- to 20-year portion of the yield curve.

For property and casualty insurers, durations of around five years can be used to match medium-term liabilities. Meanwhile, life insurers require longer duration bonds. Given the fact that munis are used to finance US Infrastructure, many insurance companies use them as a diversification to their infrastructure investments.

In the portfolios of very long-term investors such as pension funds, munis sit somewhere between Treasuries and corporate bonds, providing strong capital protection with yield uplift and diversification benefits.

Q. Can you sum up the opportunity for investors?

A. The US municipal market is a pure credit market. Although the market possesses strong average quality, the divergence between individual issuers can be profound. While historical default experience is low in comparison with similarly-rated corporate bonds, chronic underfunding of long-term liabilities is a challenge for many state and local issuers. We believe that while good opportunities for global investors remain, prudent investment in munis begins by accessing a partner dedicated to investment in the sector, and with strong capabilities in fundamental credit, portfolio and market research.

1 http://www.sifma.org/research/statistics.aspx

2 http://www.msrb.org/msrb1/pdfs/MSRB-Muni-Facts.pdf

3 Bloomberg Barclays Indices

4 Moody’s Investor Services: US Municipal Bond Defaults and Recoveries, 1970-2015, May 31, 2016

5 Bloomberg

6 https://www.federalreserve.gov/apps/fof/DisplayTable.aspx?t=l.212

The market outlook contained herein is prepared by McDonnell Investment Management, LLC (“McDonnell”) for informational purposes only. The information set forth herein is neither investment advice nor legal advice. It is presented only to provide information on investment strategies and our view on market opportunities. The data used for this presentation was obtained from publicly available reports and may include, but are not limited to, some or all of the following: internally derived databases and information, third party research, issuer-derived documents and news media reports. McDonnell believes the data to be reliable but does not make any representations as to its accuracy or completeness. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. The views expressed by McDonnell are as of the date of publication of this piece, are based on current market conditions, may fluctuate and are subject to change without notice. McDonnell cannot assure that the type of investments discussed herein will outperform any other investment strategy in the future, nor can it guarantee that such investments will present the best or an attractive risk-adjusted investment in the future. Statements of future expectations, estimates, projections and other forward-looking statements are based upon available information and McDonnell’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risk and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. There are no assurances that any predicted results discussed herein will actually occur. Past performance is no guarantee of future results.

Published in July 2017

McDonnell Investment Management, LLC

A subsidiary of Natixis Global Asset Management, L.P.,

Investment adviser registered with the U.S. Securities and Exchange Commission

18W140 Butterfield Road

Suite 1200

Oakbrook Terrace, IL 60181

www.mcdonnellinvestments.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2017 Natixis Investment Managers S.A. – All rights reserved

Hop Aboard the US Growth Engine

Hop Aboard the US Growth Engine

Loomis Sayles - Investment Outlook - April 2024

Loomis Sayles - Investment Outlook - April 2024

Natixis IM Solutions - Market Review - March 2024

Natixis IM Solutions - Market Review - March 2024

2024, A Singular Context of Volatility in the Markets?

2024, A Singular Context of Volatility in the Markets?