Energy Transition: Clean Investments for Yield-hungry Investors

Renewable energy is one of the fastest growing segment within the infrastructure market, as clean energy production represents both a compelling investment opportunity and a natural choice of asset allocation in the move towards a low carbon economy.

Key Takeaways:

- Making the shift to a low carbon world a success would require massive investments to replace fossil fuels by renewable energy sources.

- In addition to benefit from ambitious European targets, technological progress in solar panels and wind turbines has pushed down electricity production costs over the last years, leading to decreasing renewable exposure to political risks.

- Only an asset manager with strong technical, financial, legal and project management skills as well as a large network of industrial partners can successfully venture into financing renewable energy infrastructures.

Renewable energy has become one of the buzziest investment segments, increasingly attracting the interest of institutional investors alike. But 16 years ago, when Mirova made its first renewable energy investment, the term would have been recognisable to only a tiny handful of investors.

Mirova’s first foray into renewables in 2002, after winning a tender from the French government to create the first fund to support the wind energy sector in Europe, has now become a major area of expertise for the Paris-based investment house. Mirova, an affiliate of Natixis Investment Managers dedicated to responsible investment, has since undertaken more than 170 renewable energy projects, partnering with industrial companies to develop infrastructure across Europe.

Why renewables as an investment?

The rationale for renewable energy gets stronger as time goes by. Markets and societies need a substitute to fossil fuels as oil and gas are not compatible with their climate change objectives. Without efficient replacements, the world risks the worst outcomes with unknown consequences on the earth life quality.

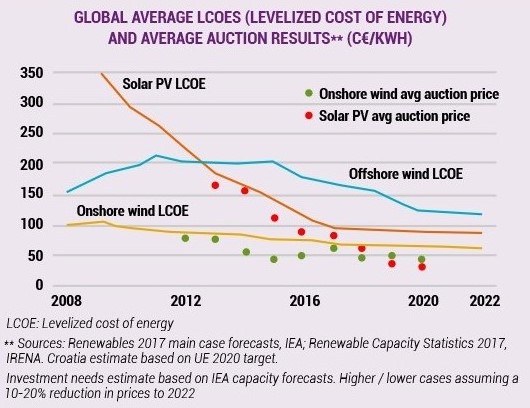

Across Europe, where the renewables industry is most advanced, outdated energy facilities are being phased out and replaced by more efficient facilities in which renewable energy is playing a bigger part. In other words, the improved competitiveness of renewable energy infrastructure has significantly decreased the inherent risks associated over the last years. As the industry develops and becomes self-sustaining, state subsidies are being phased out and substituted with market mechanisms driven by supply and demand. Construction costs of solar PV plants, for example, is now 90% less than a decade ago. In wind technology, increased competition and improved technologies have led to longer blades and taller turbines, also bringing down electricity production costs

Ever falling wind and solar production cost

As well as the economic and climate change rationale, a further driver of renewables is strong political support, particularly in the European Union. The EU has set a target for renewable energy penetration to reach 20% in total energy consumption (partly covered by electricity production) in 2020, rising to 27% in 2030. Already, renewables represent over 30% of electricity production in the EU, up from 15% in 2005.

How to access renewables sector?

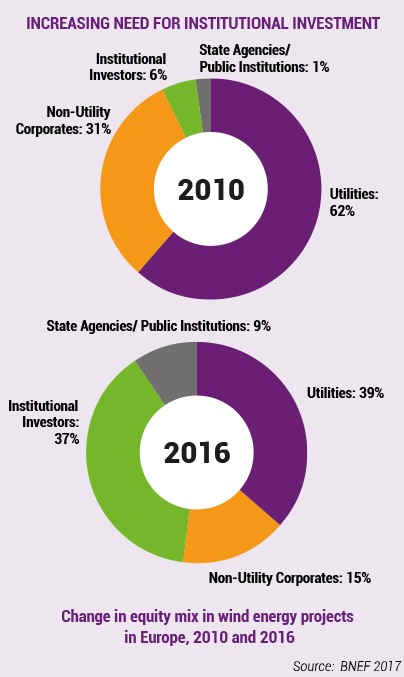

The market of renewable energy has reached an advanced stage of maturity over the last years, moving from small entrepreneurial projects to large-scale institutional ones. Major financial investors have now entered the market, looking for yield in a low-interest environment, notably insurance companies. The asset class is now source of strong performance and a strong diversification tool for institutional investors who understood their potential and play a greater role in meeting the financing needs of renewable energy infrastructures.

But even for savvy institutional investors, becoming directly part of the renewables story is not easily feasible without relying on external experts. Building a wind farm or energy storage facilities requires technical and financial know-how and experience, as well as project management skills. With investment sizes at between $5m and $50m a project, corralling these resources for single projects is not likely to be justified.

Mirova attracts capital from large numbers of investors (over $500m raised and deployed to date ) and pools it to make equity and mezzanine climate infrastructure investments across European countries. It mainly invests in mature technologies (solar photovoltaic, wind, hydro) at ready-to-build or operating stages, ensuring that capital can be deployed rapidly and thanks to a dynamic and liquis deconsart market, allow payback times for investors that are typically much shorter than for investors in other infrastructure assets which construction can last for years compared to months for renewables.

While most investments to date have been in renewable energy generation infrastructure, Mirova increasingly invests in its natural expansion assets: energy storage and electric mobility. In other words, it has spread its remit to energy transition, which aims to foster necessary long-term change in energy systems to support a decentralised production base.

Each project involves a long-term partnership – in joint venture with industrial companies and utilities to ensure alignment of interests. The assets that are created through these partnerships have a lifetime of about 25 years, but Mirova will seek to sell them within 7-10 years in order to return capital and profits to investors. In the meantime, investors receive revenues from the ongoing operation of the asset.

A package of skills

To succeed in this complex and increasingly competitive sector takes a range of financial and technical skills, plus a large industrial network to draw from, to both source and implement deals.

Every member of Mirova’s 10-strong renewable energy team has a robust background in renewable energy, as well as core skills such as project financing, deal sourcing and structuring, asset management. The investment team is supported by a dedicated risk, legal, compliance and ESG research team to ensure the quality of its investment and risk management processes

These skills and experience lead to good industrial relationships. And good industrial relationships lead to strong pipelines of deals, through referrals and repeat transactions.

The development of trust with industrial partners over a number of years and numerous transactions, allows Mirova to take on projects others may consider too complex to structure or too risky. With the support from trusted partners, the risks are better understood and managed, and greater rewards are available to all parties.

Skill and experience can also help reduce the costs of operations, from reduced legal fees to maintenance contracts optimization or refinancing of plants.

J-curve mitigation

Returns from renewable energy projects are different from private equity in nature, as Mirova’s strategy to invest in greenfield projects which are quickly operational or even directly in brownfield projects or through mezzanine, enables to quickly enhance value and generate cash flow to allow early repayment to investors and mitigation the J-curve effect.

Overall, the strategy aims to delivers return of 8%-9% net to investors over the 10-15 year lifetime of a fund, with a 5% annualised cash yield as underlying assets rely on a regular cash-generating business model1. These returns and timeframes tend to suit insurers, endowments, wealth funds and pension funds.

For insurers, the all-important cost of capital under the EU’s Solvency II regime is extremely low, with an SCR of about 15% (using a look through analysis). This compares to an SCR of 49% for private equity and 30% for infrastructure.

A world of opportunities

The core investments – solar and wind farms – still provide good returns, but investment performance is coming under pressure in Western European markets, which are maturing and increasingly viewed as low risk and a differentiated strategy is required to continue to search for strong return.

Mirova sees more financial upside in five key areas:

- Partnerships with industrials and utilities in European projects, leveraging on existing relationships and framework agreements to secure pipelines of future projects. Utilities and developers continue relying on financial players to help them build their projects and deleverage their balance sheet, and they value the deal execution certainty that Mirova, being a specialist in the sector, can provide even on complex deal structures.

- OECD countries outside Western Europe. Geographical extension in the medium term is likely to lead to more deals in countries such as Canada, Australia and the US, where some of Mirova’s industrial partners already operate and are asking for financial support.

- Early stage projects. On the face of it early, or development stage, projects involve more risk and higher returns. The pre-construction stage is all about getting land permits, dealing with public enquiries, taking part in environmental studies and other set-up activities that eat up time and resources. Experienced operators can assess the likelihood of success and avoid early-stage projects which have low chances of success and are ready to take on most of the development risk. In effect, higher returns are available for investors without actually taking more risk.

- Energy storage. The energy storage market over 2016-2030 is predicted (by Bloomberg New Energy Finance) to mirror the photovoltaic solar trajectory over the 2000-2015 period, which doubled six times in 15 years. The cost of batteries is forecast to decline by as much as 35% over the next five years. This can mitigate significantly the intermittence of renewables. Mirova has been investing in storage projects since 2012.

- Advanced mobility. Meanwhile, advanced mobility, or charging for electric vehicles, is a major preoccupation of the auto industry. Mirova has trusted partners already working in this field and is preparing projects with number of them. These projects are nothing but decentralised renewable energy projects with storage capabilities thus a convergence with the renewable energy sector, and project finance model is starting to apply to this fast-growing industry.

Published in March 2018

MIROVA

Filiale de Natixis Asset Management

Société Anonyme

Capital: €7 641 327.50

Agréé par l’Autorité des Marchés Financiers (AMF) sous le numéro GP 02014.

RCS Paris n° 394 648 216

21 quai d’Austerlitz 75013 Paris France

www.mirova.com

Ostrum Asset Management

An affiliate of Natixis Investment Managers

Société Anonyme

Capital €50 434 604.76

Agréé par l’Autorité des Marchés Financiers (AMF) sous le numéro GP 90-009

RCS Paris n°329 450 738

Immeuble Elements

43 avenue Pierre Mendès France

75013 Paris

www.ostrum.com

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

Immeuble Elements

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2018 Natixis Investment Managers S.A – All rights reserved

Equity Infrastructure: Decorrelated, Long-term Income

Equity Infrastructure: Decorrelated, Long-term Income