Mid-Market Private Equity: 2.0

Solving the challenge of geographical diversification

Mid-market private equity has grown in popularity as investors seek to invest in the high-growth companies that drive economies. The relatively small scale of deals compared with the large buyout funds means the focus of mid-market private equity is local. That is, the segment is dominated by domestic private equity funds investing primarily in domestic companies.

Investing in single countries or regions can make sense – the closer you can get to investee companies, the more likely you are to select the ones with the greatest potential. However, the model lacks diversification; investors are potentially exposed to countries and regions which have structurally slow growth or suffer from geopolitical problems. Exposure to companies in a larger number of countries, across geographic regions, strengthens diversification, potentially providing protection against underperforming national economies and benefiting from faster-growing countries.

But is it possible to both invest locally and, at the same time, have a global focus?

Mid-market opportunities

Before we answer that, let’s consider why investors are attracted to mid-market private equity.

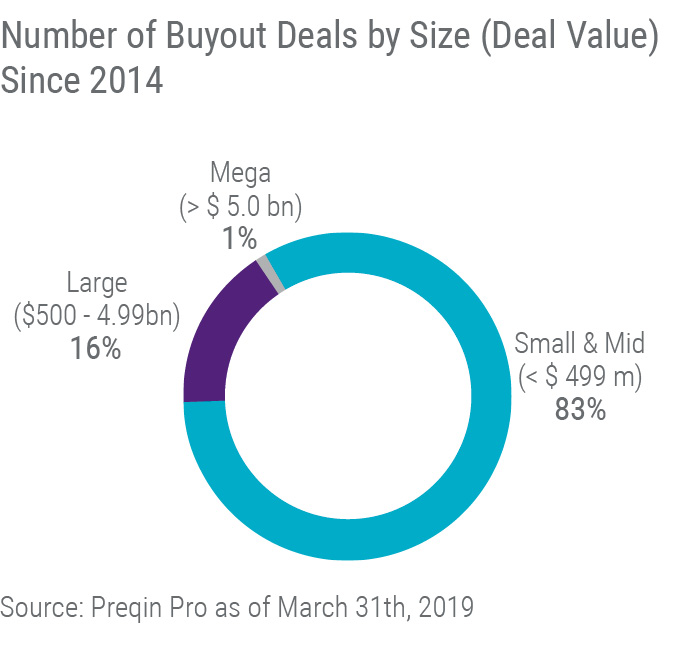

The small- and mid-market private equity sector has historically provided outperformance across most phases of the economic cycle. Investors also like the fact that they usually pay lower entry multiples than for larger deals. In addition, it is a highly active segment with strong deal flow. In fact, 83% of the deals closed since 2014 were classified as mid-market.

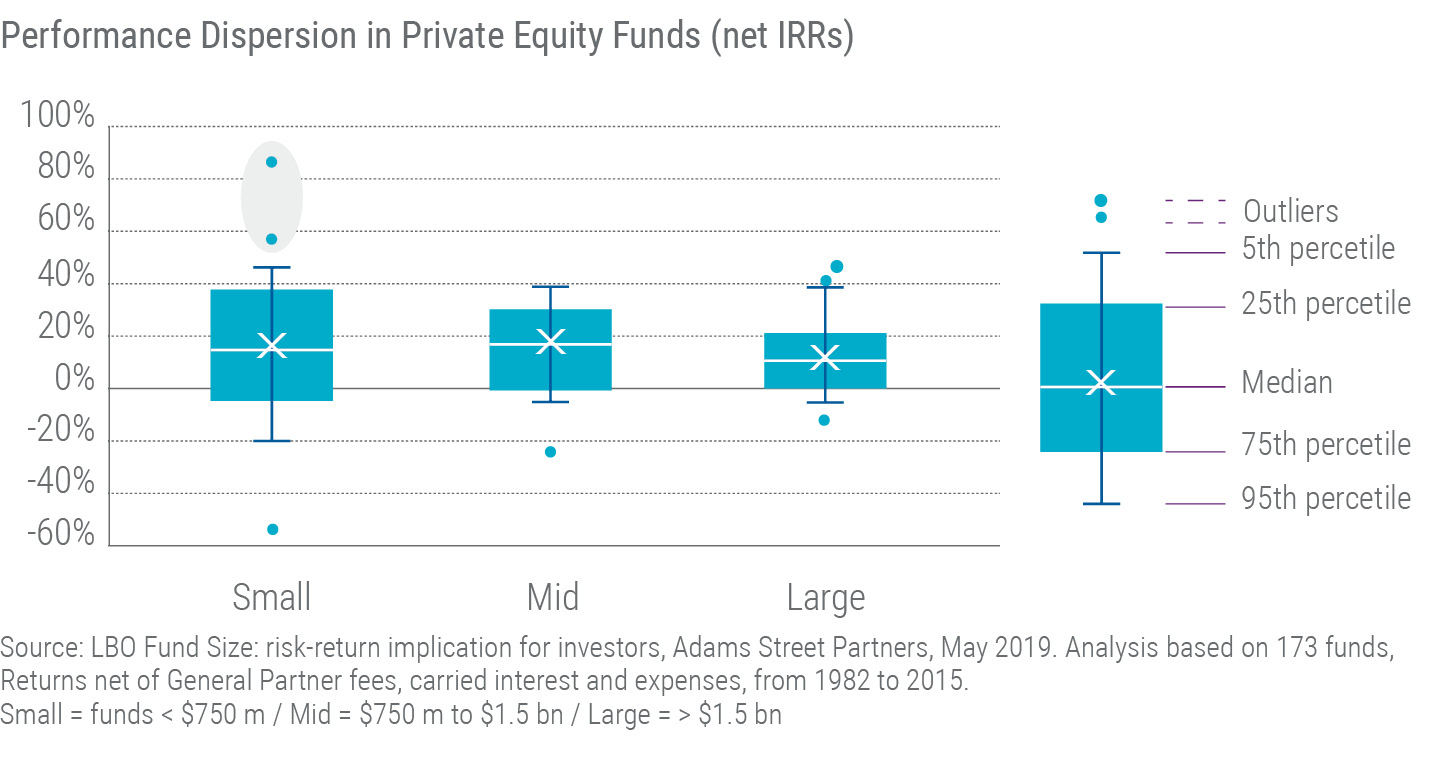

The mid-market offers an attractive risk-return profile, with greater dispersion of returns but opportunity for higher alpha. The dispersion of returns emphasizes the need to access the segment through skilled managers.

The value from mid-market deals comes from various sources, including enhancing the company’s management team, widening the company’s geographic scope and product range, and making add-on acquisitions. The strategy is better at adapting to changing market conditions than larger deals because smaller companies can be refocused more rapidly. In addition, the mid-market reduces risk by relying less on leverage to generate returns than large-cap deals. There is a wider array of exit opportunities in the mid-market too, including selling a portfolio company to a larger fund or peer-group competitor.

The case for geographic diversification

So the mid-market has great potential to create superior value. “But we believe that geographical diversification can improve the offer still more,” says David Arcauz, managing partner at Flexstone.

“The risks of not diversifying are growing,” he notes. Amid arguably the longest economic recovery in history, the risks to the downside are growing. Investors are better placed to weather an economic downturn if they operate a geographically-diversified portfolio rather than a portfolio of companies based in a single country or region. Equally, a reversal in the low interest rate environment will impact private equity returns, particularly on highly-leveraged deals. And it may be difficult to predict which jurisdictions will raise rates the fastest and longest.

Then there’s the macro-economic environment, with trade wars and political uncertainty affecting some countries and regions more than others. “We think institutional investors should be allocating to private equity opportunities all over the world, not into a limited handful of countries and certainly not in a single country,” says Arcauz.

Regional diversity

The differences between countries are not limited to economics; the private equity environment varies depending on the country and region too.

In Europe, for instance, private equity markets are driven by smaller deals, while in the US average fund sizes are much larger. Meanwhile, since 2016 in Europe, debt levels for mid-market deals have trended markedly towards levels similar to the levels observed in the US, more or less stable, representing half of the enterprise values in average.

Jimmy Hsu, Singapore-based managing director at Flexstone: “From a regional, cultural standpoint only the US is homogenous. Europe and Asia are both fragmented so you need a local partner in each region to navigate the local landscapes.” Each country in Asia and Europe has different codes, cultures, structures and laws. It is possible to take a blanket approach and target only larger, highly-visible companies that operate across Europe or across Asia but this risks missing the larger value created by fast-growing, lesser-known enterprises in niche sectors.

David Arcauz, Geneva-based managing partner at Flexstone, says: “Europe’s capital markets are dominated by smaller companies, and not many of these are listed. So if you want exposure to SMEs in Europe, you need to invest through a private equity strategy.” The cultural homogeneity of the US allows for easier comparison of target companies, But the sheer volume and breadth of the US market provides further opportunities to diversify a global mid-market portfolio. “The US mid-market is huge,” says Nitin Gupta, New York-based Flexstone’s managing partner. “You can target a range of different deal sizes and types within this segment in the US, and diversify the portfolio by sector too.”

Global presence, local focus

To unearth the most promising mid-market companies worldwide requires a global team with local expertise in the world’s major regions: US, Europe, and Asia. Accessing a global opportunity set necessitates feet on the ground, and proximity to companies and deal networks. With access to the best-performing mid-market funds in high demand, relationships with managers is critical. None of this can be achieved by operating remotely.

Flexstone Partners, an affiliate of Natixis Investment Managers, was conceived expressly to bring a global perspective to the private equity mid-market. Constructed by the combination of three existing Natixis affiliates –Caspian Private Equity, Euro-PE, and Eagle Asia – its management team has decades of experience in the mid-cap buyout and growth segment. Partnering with leading small and mid-cap private equity funds1, Flexstone has allocated to more than 400 funds worldwide, seating on many advisory boards.

A la carte investing

Using Flexstone’s a la carte menu for investment strategy, research and selection, structuring, tax, accounting and reporting, investors can create globally-diversified portfolios that are tailored to their particular needs.

“Clients come in with all different shapes and forms of needs,” says Nitin Gupta, “some want certain geographical exposures to dovetail with existing exposures in their portfolios. For others, the priority may be to take more risk, perhaps by investing with emerging managers or expending on a new region. No two clients are the same.”

Flexstone’s approach allows investors to diversify by region, but also by manager type, sector and size of deal. As a result, many of Flexstone’s mandates are executed through separate accounts. This means the structuring of the investments is important. “In some countries, one of the first questions is often how to structure deals, not what deals the investor is looking for,” says David Arcauz. “Our first job is to guide investors on structuring.” The resulting portfolios respond to the objectives of clients, with assets matching these objectives.

In Asia, for instance, investors often prefer funds of funds. “Asian clients are often looking for revenue growth and margin expansion so high-alpha funds of funds may be suitable,” says Jimmy Hsu. “We can get access to the high-performing funds that tend to close quickly.”

Whatever the geographic allocation, investors receive consolidated reports on the worldwide portfolio, which they can slice and dice for their own reporting needs.

Conclusion

Some institutional investors have the resources and experience in private equity investing to make their own global allocations. Many others, however, would like to tap the historically high returns from the private equity mid-market, but seek a partner to steer them through the complexities and to achieve better diversification.

This is where a global private equity adviser, with a local presence on the ground in all the major regions of the world, can prove its worth.

1 Leading private equity funds according to Flexstone Partners' Due Diligence process and criteria

Published in October 2019

Flexstone Partners

An affiliate of Natixis Investment Managers

Flexstone Partners, SAS – Paris

Investment management company regulated by the Autorité des Marchés Financiers. It is a simplified stock corporation under French law with a share capital of 1,000,000 euros Under n° GP-07000028 –Trade register n°494 738 750 (RCS Paris)

5/7, rue Monttessuy,

75007 Paris

www.flexstonepartners.com

Flexstone Partners, SàRL – Geneva

Independent (unregulated) asset manager, under Swiss Federal Act on Collective Investment Schemes (“CISA”), supervised by Commission de haute surveillance de la prévoyance professionnelle (“CHS PP” and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”) under Anti Money Laundering requirements. It is a limited liability company with a share capital of 750 000 CHF.

Trade register n° CH-660-0180005-1

8 chemin de Blandonnet

Vernier 1214 Geneva

Switzerland

Flexstone Partners, LLC - New York

Delaware corporation, registered with the United States Securities and Exchange Commission as an investment adviser

28th floor of 745 Fifth Avenue, New York, NY 10151.

Flexstone Partners, PTE Ltd - Singapore

61 Robinson Road, #08-01A Robinson Centre

Singapore 068893

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2019 Natixis Investment Managers S.A. – All rights reserved

KEY TAKEAWAYS:

- Exposure to mid-market companies across a large geographical area can strengthen diversification in a private equity portfolio. Gaining global exposure to the mid-market is rare

- Each of the main three global regions – Europe, US and Asia – has different economic drivers and different risk profiles. Exposure to all three is preferable to manage risk and enhance returns

- To unearth the best mid-market companies worldwide requires a global team with local expertise in the world’s major regions. Accessing a global opportunity set necessitates feet on the ground, and proximity to companies and deals

Resources

Mid-market private equity has grown in popularity as investors seek to invest in the high-growth companies that drive economies. The relatively small scale of deals compared with the large buyout funds means the focus of mid-market private equity is local. That is, the segment is dominated by domestic private equity funds investing primarily in domestic companies.

Investing in single countries or regions can make sense – the closer you can get to investee companies, the more likely you are to select the ones with the greatest potential. However, the model lacks diversification; investors are potentially exposed to countries and regions which have structurally slow growth or suffer from geopolitical problems. Exposure to companies in a larger number of countries, across geographic regions, strengthens diversification, potentially providing protection against underperforming national economies and benefiting from faster-growing countries.

But is it possible to both invest locally and, at the same time, have a global focus?

Mid-market opportunities

Before we answer that, let’s consider why investors are attracted to mid-market private equity.

The small- and mid-market private equity sector has historically provided outperformance across most phases of the economic cycle. Investors also like the fact that they usually pay lower entry multiples than for larger deals. In addition, it is a highly active segment with strong deal flow. In fact, 83% of the deals closed since 2014 were classified as mid-market.

The mid-market offers an attractive risk-return profile, with greater dispersion of returns but opportunity for higher alpha. The dispersion of returns emphasizes the need to access the segment through skilled managers.

The value from mid-market deals comes from various sources, including enhancing the company’s management team, widening the company’s geographic scope and product range, and making add-on acquisitions. The strategy is better at adapting to changing market conditions than larger deals because smaller companies can be refocused more rapidly. In addition, the mid-market reduces risk by relying less on leverage to generate returns than large-cap deals. There is a wider array of exit opportunities in the mid-market too, including selling a portfolio company to a larger fund or peer-group competitor.

The case for geographic diversification

So the mid-market has great potential to create superior value. “But we believe that geographical diversification can improve the offer still more,” says David Arcauz, managing partner at Flexstone.

“The risks of not diversifying are growing,” he notes. Amid arguably the longest economic recovery in history, the risks to the downside are growing. Investors are better placed to weather an economic downturn if they operate a geographically-diversified portfolio rather than a portfolio of companies based in a single country or region. Equally, a reversal in the low interest rate environment will impact private equity returns, particularly on highly-leveraged deals. And it may be difficult to predict which jurisdictions will raise rates the fastest and longest.

Then there’s the macro-economic environment, with trade wars and political uncertainty affecting some countries and regions more than others. “We think institutional investors should be allocating to private equity opportunities all over the world, not into a limited handful of countries and certainly not in a single country,” says Arcauz.

Regional diversity

The differences between countries are not limited to economics; the private equity environment varies depending on the country and region too.

In Europe, for instance, private equity markets are driven by smaller deals, while in the US average fund sizes are much larger. Meanwhile, since 2016 in Europe, debt levels for mid-market deals have trended markedly towards levels similar to the levels observed in the US, more or less stable, representing half of the enterprise values in average.

Jimmy Hsu, Singapore-based managing director at Flexstone: “From a regional, cultural standpoint only the US is homogenous. Europe and Asia are both fragmented so you need a local partner in each region to navigate the local landscapes.” Each country in Asia and Europe has different codes, cultures, structures and laws. It is possible to take a blanket approach and target only larger, highly-visible companies that operate across Europe or across Asia but this risks missing the larger value created by fast-growing, lesser-known enterprises in niche sectors.

David Arcauz, Geneva-based managing partner at Flexstone, says: “Europe’s capital markets are dominated by smaller companies, and not many of these are listed. So if you want exposure to SMEs in Europe, you need to invest through a private equity strategy.” The cultural homogeneity of the US allows for easier comparison of target companies, But the sheer volume and breadth of the US market provides further opportunities to diversify a global mid-market portfolio. “The US mid-market is huge,” says Nitin Gupta, New York-based Flexstone’s managing partner. “You can target a range of different deal sizes and types within this segment in the US, and diversify the portfolio by sector too.”

Global presence, local focus

To unearth the most promising mid-market companies worldwide requires a global team with local expertise in the world’s major regions: US, Europe, and Asia. Accessing a global opportunity set necessitates feet on the ground, and proximity to companies and deal networks. With access to the best-performing mid-market funds in high demand, relationships with managers is critical. None of this can be achieved by operating remotely.

Flexstone Partners, an affiliate of Natixis Investment Managers, was conceived expressly to bring a global perspective to the private equity mid-market. Constructed by the combination of three existing Natixis affiliates –Caspian Private Equity, Euro-PE, and Eagle Asia – its management team has decades of experience in the mid-cap buyout and growth segment. Partnering with leading small and mid-cap private equity funds1, Flexstone has allocated to more than 400 funds worldwide, seating on many advisory boards.

A la carte investing

Using Flexstone’s a la carte menu for investment strategy, research and selection, structuring, tax, accounting and reporting, investors can create globally-diversified portfolios that are tailored to their particular needs.

“Clients come in with all different shapes and forms of needs,” says Nitin Gupta, “some want certain geographical exposures to dovetail with existing exposures in their portfolios. For others, the priority may be to take more risk, perhaps by investing with emerging managers or expending on a new region. No two clients are the same.”

Flexstone’s approach allows investors to diversify by region, but also by manager type, sector and size of deal. As a result, many of Flexstone’s mandates are executed through separate accounts. This means the structuring of the investments is important. “In some countries, one of the first questions is often how to structure deals, not what deals the investor is looking for,” says David Arcauz. “Our first job is to guide investors on structuring.” The resulting portfolios respond to the objectives of clients, with assets matching these objectives.

In Asia, for instance, investors often prefer funds of funds. “Asian clients are often looking for revenue growth and margin expansion so high-alpha funds of funds may be suitable,” says Jimmy Hsu. “We can get access to the high-performing funds that tend to close quickly.”

Whatever the geographic allocation, investors receive consolidated reports on the worldwide portfolio, which they can slice and dice for their own reporting needs.

Conclusion

Some institutional investors have the resources and experience in private equity investing to make their own global allocations. Many others, however, would like to tap the historically high returns from the private equity mid-market, but seek a partner to steer them through the complexities and to achieve better diversification.

This is where a global private equity adviser, with a local presence on the ground in all the major regions of the world, can prove its worth.

Published in October 2019

Flexstone Partners

An affiliate of Natixis Investment Managers

Flexstone Partners, SAS – Paris

Investment management company regulated by the Autorité des Marchés Financiers. It is a simplified stock corporation under French law with a share capital of 1,000,000 euros Under n° GP-07000028 –Trade register n°494 738 750 (RCS Paris)

5/7, rue Monttessuy,

75007 Paris

www.flexstonepartners.com

Flexstone Partners, SàRL – Geneva

Independent (unregulated) asset manager, under Swiss Federal Act on Collective Investment Schemes (“CISA”), supervised by Commission de haute surveillance de la prévoyance professionnelle (“CHS PP” and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”) under Anti Money Laundering requirements. It is a limited liability company with a share capital of 750 000 CHF.

Trade register n° CH-660-0180005-1

8 chemin de Blandonnet

Vernier 1214 Geneva

Switzerland

Flexstone Partners, LLC - New York

Delaware corporation, registered with the United States Securities and Exchange Commission as an investment adviser

28th floor of 745 Fifth Avenue, New York, NY 10151.

Flexstone Partners, PTE Ltd - Singapore

61 Robinson Road, #08-01A Robinson Centre

Singapore 068893

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2019 Natixis Investment Managers S.A. – All rights reserved

Flexible Access to Private Equity

Flexible Access to Private Equity

How to Eradicate the J-Curve in Private Equity?

How to Eradicate the J-Curve in Private Equity?

Hop Aboard the US Growth Engine

Hop Aboard the US Growth Engine