Corporate Loans Come of Age

Key Takeaways:

- Compared to investment grade bonds, corporate loans provide a sizeable yield pick-up and excellent risk-return characteristics relative to other credit instruments

- Loomis Sayles and Natixis Asset Management share similarities in how they implement their corporate loan strategies. Both are income-driven, invest only in senior, secured loans, and rely on large research teams. The former focuses primarily on US corporate loans while the latter targets European loans.

- As interest rates in the US and elsewhere rise, loans offer protection from duration risk

Resources

Holders of fixed income securities are mindful, to say the least, of the risks of rising rates. But they have options. Few will jettison their bond holdings, but some are complementing them with income-producing securities that are less sensitive to interest rates. These include corporate bank loans.

Why bank loans?

The bank loans market in the US is now worth more than $900bn1, substantially above its pre-crisis level of a little over $500bn. The more youthful European loans market is rising too, with volumes in the leveraged loans market having expanded every year since 2008.

From an investor’s viewpoint, the rationale for corporate loans is compelling. Compared to investment grade bonds, loans provide a sizeable yield pick-up. Senior, secured loans are particularly attractive to institutional investors, who are keenly aware of the risk-return trade-off. Few institutional asset owners are willing to seek additional return in their bond portfolios at the risk of a blow-up which could reduce returns, or worse, lead to capital losses. Senior, secured loans, have first call on a company’s assets in the case of insolvency.

They are created with institutions in mind: bankers designed loans to sit on the bank’s own balance sheet and perform a core role as a steady returner with low volatility.

For many institutional investors, particularly those with long-term liabilities, an asset’s sensitivity to interest rate risk is a critical aspect of portfolio management. Bank loan yields are based on floating interest rates, which means there is no duration risk. This contrasts with high yield bonds and emerging market sovereign debt, two asset classes with comparable yields, but with high sensitivity to interest rates.

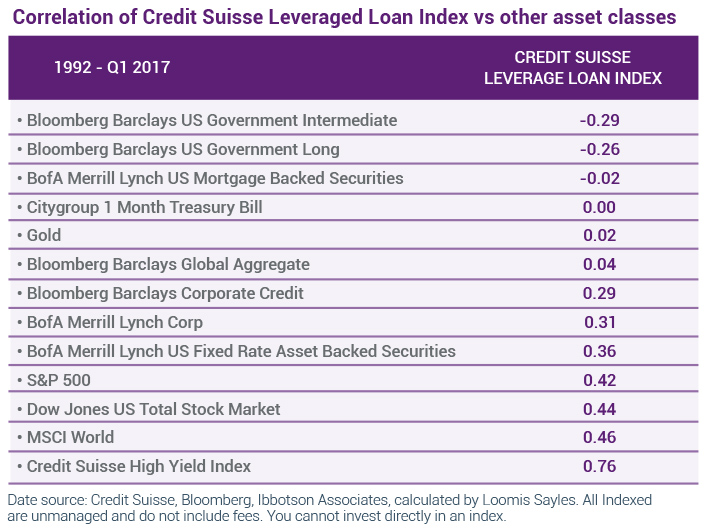

Bank loans are also perennial diversifiers in portfolios, generally outperforming when other asset classes are underperforming. Low correlation with other major asset classes is particularly marked in relation to developed market government bonds and broad corporate bond indices such as Bloomberg Barclays Corporate Credit.

Finally, it is of comfort to corporate loan investors to know that comparatively few loans are due to mature in the next three years. This significantly reduces the chances of defaults. As of 30 September 2017, for instance, just $0.3bn of loans, or 0.3% of the index, is due to mature, and only $15bn remains in 2018. So even if all of these companies were to default, the impact on corporate loan portfolios would not be material.

A tale of two strategies

While corporate loans offer inherent advantages to investors, loan investment strategies can take many forms, some more differentiated than others. Let’s look at two well-regarded strategies – one managed by Loomis Sayles and the other by Ostrum Asset Management.

The two investment firms, both affiliates of Natixis Investment Managers, share some similarities in how they implement their corporate loan strategies. Both invest only in senior, secured loans, and both rely on large research teams with specialist knowledge of the loans market and deep credit analysis of the relevant companies and markets.

One of the key differences is that while Loomis Sayles focuses primarily on US corporate loans, Ostrum Asset Management (Ostrum AM) targets European loans.

The US market, whose history goes back to the late 1980s is considerably more mature, and investors can benefit from decades of data and a deep and liquid market. Europe’s loan market, on the other hand, only got going in the 2000s.

After the peak of 2007 and the financial crisis, the European market started to rebound in 2010, driven by the global recovery, substantial private equity dry powder and the refinancing of older transactions. The market has accelerated since 2013, with M&A activity and the resurgence of CLOs. It is, by Natixis AM estimates, still only one-sixth of the size of the US market, so may not offer quite the same levels of liquidity. However, the European market offers untapped opportunities for investors with deep analysis capabilities, and is probably a little earlier in the credit cycle than the US.

There are advantages and disadvantages to investing in either market, and both Natixis AM and Loomis Sayles have adapted their strategies to maximise the former and minimise the latter.

Loomis Sayles: credit quality first, and foremost

Loomis Sayles’ approach to the corporate loan market is characterised by a conservative philosophy. “Institutions care about return versus risk, not return at any risk,” says John Bell, portfolio manager of the Loomis Sayles’ Senior Loan strategy.

Bell, one of three portfolio managers for the strategy, believes in a higher quality bias than the wider loan index over most of the credit cycle. The managers also impose strict portfolio discipline with intense focus on individual credit quality. Their aim is to outperform the S&P/LSTA U.S. BB Ratings Loan Index over full credit cycles.

Most corporate loan funds can allocate up to 20% to non-loan instruments such as high-yield bonds. Loomis Sayles believes in a pureplay approach to first priority syndicated bank loan market, entailing no high-yield or second lien exposure at all. This fits with its aim of gearing its strategy for this market to institutional investors interested in higher return per unit per risk, rather than the highest return irrespective of risk.

In an asset class where there is much more potential downside than upside, the security afforded by higher-quality assets is paramount. In that context, putting high-yield into the mix, as some investment strategies in this market do, is an inefficient way to increase return vs risk.

The loans selected tend to be at the higher end of the rating spectrum. “If you put bank loan managers in a continuum by rating, we would be at the most conservative end,” says Bell. The managers’ preferred BB-rated loans tend to be less volatile and have higher Sharpe ratios (that is, higher returns vs risk taken) than lower-rated loans. In the last full business cycle, from December 2001 to June 2009, BB loans returned 3.17% a year versus just 0.76% for CCC-rated loans, even though the risk of CCC loans is more than twice that of BB-rated loans.

Teams and screens

Credit research is the bedrock of the conservative Loomis Sayles investment process. Bell and co-fund manager Kevin Perry have worked together since 1989, while the third portfolio manager, Michael Klawitter, has 19 years’ experience in the industry. The trio solely manage bank loans and are not required to analyse other forms of credit, as is the case in some investment houses. The importance of this long experience of working together is that the decision-making process is fully evolved, with few disagreements.

A key differentiator from industry norms is how the Loomis Sayles portfolio managers use the firm-wide resources. They eschew the standard straight-line structure of analysts reporting to fund managers, who report upwards to a chief investment officer. “Working in silos doesn’t work if you want to do serious credit analysis,” says Kevin Perry. “Silos tend not to talk to each other. Our credit research is organised by industry and our analysts don’t just look at bank loans.” In fact, the 50-strong team has expertise across the capital structure, from convertibles to investment grade, enabling flows of relevant information and cross-fertilisation of ideas.

For a loan to even get to the credit analysis stage, it must successfully pass two screens. The first screen considers near-term credit concerns. Given that bank loans are usually paid off early, if there is a possible negative credit event in the next year or two, the opportunity is immediately passed up. The second assesses the value of the company to make sure it is worth twice the loan amount. Passing that test ensures that the company would have to shrink by 50% to get close to impairing the loan value.

Once a loan opportunity passes these two screens, the centralised research group examines the credit metrics, including management, exogenous threats and covenants. If the potential return and the pricing are also reasonable, the loan is considered for the portfolio.

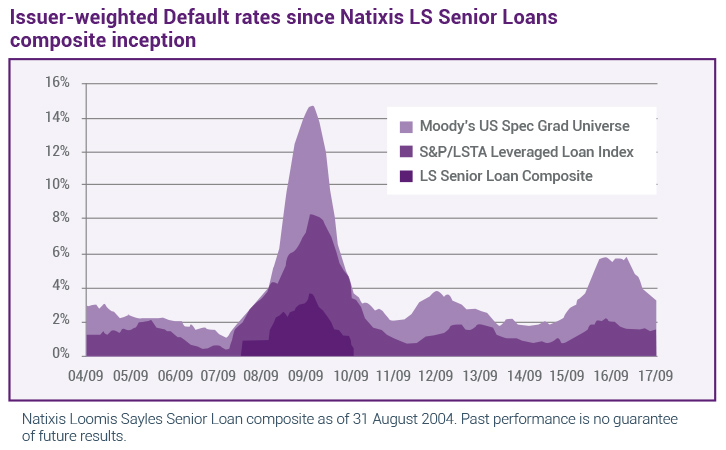

The result of this process is considerably fewer defaults than for the broader universe of bank loans.

Data source: Moody’s, S&P/LCD, and State Street (Fund custodian), calculated by Loomis Sayles through 30 September 2017. Moody’s US Speculative Grade Trailing 12-month Default Rate is calculated as the number of defaults in the rated universe divided by the number of issuers that could have defaulted during the period. S&P/LCD Bank Loan default rate is calculated as the number of defaults over the last twelve months divided by the number of issuers in the S&P/LSTA Index at the beginning of the twelve-month period. Natixis Loomis Sayles Senior Loan composite default rate is calculated as the cumulative percentage default rate (number of defaulted issuers in the portfolio divided by the number of issuers in the portfolio at the beginning of each month) over the last 12 months. Moody's US Speculative-grade Trailing 12-month Default Rate Index is an unmanaged index which measures the percentage of speculative-grade companies (those with ratings below triple-B) in the US that are in distress. Moody's is a provider of independent credit ratings, research and financial information to the capital markets. Please see Performance, Reference Information and Additional Notes slides for additional information.

Since 2004, 252 loans in the reference index have defaulted, but Loomis Sayles only bought 45 of them, of which 33 were sold before default. Recent performance has been better still. “We have not had a bankruptcy in the portfolio since October 2009,” says Perry.Portfolio construction – with style

The strict portfolio construction rules are designed to minimise risk of loss. First, the portfolio is well-diversified, with 200-300 loans held on average. “Portfolios are more diversified than equity ones because specific risk is not your friend in the bank loan space,” says Bell. On the other hand, some portfolios have up to 500 names. “We think that’s too many, it’s hard to have a specific style with that number,” he adds. Other rules include owning generally no more than 10% of loans sourced from one industrial sector.

The sell process is stringent, with monitoring taking place throughout the day. If confidence is lost in a credit then it is likely to be jettisoned from the portfolio. However, if there is high conviction, the loan may be retained even if it is in default. “There is no style drift, even if there is a crisis,” says Bell. “We don’t get more or less conservative. We won’t panic and sell – if we do sell in haste, we may not be able to buy it back. “During the financial crisis, we made our money back the following year. Holding loans through volatility was the right thing to do. People certainly didn’t want to sell once values came bouncing back.”

Natixis AM: adding country diversification to the mix

Although there are similarities with Loomis Sayles’ strategy, Natixis AM takes a largely different approach to investing in loans. Its principal area of focus is the European leveraged loan market. The loans it purchases underpin the leveraged buyout market, which is a diversified market which exists primarily to facilitate purchases of companies by private equity firms.

Although in the US the volume of corporate loans is high, allowing considerable diversification, in Europe there is the advantage of country diversification. A variety of jurisdictions and economies spanning the -Nordic countries-, Germany, France, Spain, Italy, the UK and the Netherlands all have deep ponds for loan investors to fish in. Add to that industry diversification and the pool of European leveraged loan assets can provide significant portfolio diversification.

Natixis AM invests in senior bank loans in both the primary and secondary markets. Given that the secondary market is relatively illiquid, Natixis AM largely employs a “buy and hold” strategy. It holds the loans in two types of funds: a Collateralised Loan Obligation (CLO) Fund, and an unlevered fund, which is a closed structure, similar to a private equity fund.

No mezz, no fuss

Natixis AM’s strategy is to invest in non-rated loans as well as private and publicly rated loans. The process of selecting -assets in this diverse universe is necessarily robust, with the safety of principal the prime consideration. The investment process is underpinned by in-depth analysis by dedicated credit analysts, and selection/portfolio construction by the portfolio managers with assets - from both the primary and secondary markets.

In common with the Loomis Sayles strategy, Natixis AM focuses solely on senior loans secured on the assets of the borrowers. The strategy does not consider subordinated or mezzanine debt in private equity deals. “We don’t think we are paid for the higher risk,” says Jean-Luc Simon, head of private debt at Natixis AM. “The recovery rate is very low in subordinated debt and in terms of mezzanine, a European fund with 10 names (the asset pool is quite limited in Europe) exposes you to very high risk.”

Natixis AM’s strategy excludes small-cap companies. Although some funds are willing to invest in the debt of companies with very small market capitalisations, Natixis AM believes the size of the debt and of the issuer must ensure sufficient liquidity for loans to be sold when necessary.

Know-how and networking

A disciplined asset selection process is possible only with constant interaction between managers and analysts, says Simon. Natixis AM’s corporate loan strategy is managed by eight investment professionals, each with more than 20 years of experience. The team has invested in private placements totalling €857m since 2014. Five credit analysts are fully dedicated to the senior secured and private debt loans strategy and benefit from the research of 13 corporate analysts specialised by industry. This is a rare feature in the European loan fund management industry.

The three fund managers hold the voting power in the Natixis AM investment committee, where there must be unanimity over portfolio decisions. The monitoring committee can meet at any time to consider amendments to a loan, such as a refinancing, or to decide to sell an asset where credit performance is weakening.

When deciding whether to invest, a quantitative process is used to estimate the potential return on the transaction compared with other, similar transactions and the impact on the whole portfolio.

The Natixis AM credit teams’- long experience also comes in handy for sourcing transactions: the Natixis AM strategy is exposed to a wide range of credit types, from high yield to non-investment grade, with the credit quality ranging from BB+ to B-. This requires a strong network to source the assets and cover the whole market.

Focus on risk vs reward

No loan can exceed 3% of the assets in the Natixis AM strategy and no industry can represent more than 25% of the strategy. There is also a cap on loans originating in southern Europe to allay investors’ fears about another eurozone crisis.

But the key metric for Natixis AM is the risk-reward equation. “We have seen loans at just 300bps above Euribor (the European short-term lending rate) and we think that’s too low,” says Simon. “Equally, we may exit loans where the spreads have tightened to take advantage of loans at higher spreads,-we are cautious to select the assets with the best spread per unit of leverage”.

Monitoring must be active across the whole portfolio, he says. The European leverage loan universe is not as liquid as the US leveraged loan universe, so proactive portfolio management is required. The credit researchers and analysts stay close to each of the names in the portfolio, so they can rapidly highlight risks and underperformance in order that the portfolio managers can make timely decisions about whether to sell or reduce holdings. Since the launch of the senior secured loan strategy at Natixis AM, the portfolio of loans has had a zero default track record.

Who it’s for

The strategy has a maturity of seven to 10 years, so investors must be prepared to lock up their capital for that period of time. However, interest on loans and repayments is paid to investors every quarter and, after the initial three-year investment period, the loans will be steadily repaid, allowing capital to be returned to investors. Which means in practice that the actual average duration of the strategy is between five to 7 years. The targeted return for Natixis AM’s corporate loans strategy is Euribor + 400 bps.

The repayments take place regularly as companies refinance themselves to take advantage of lower rates, or to grow in new markets and make acquisitions. They may also pay back the capital from cashflow. Equally, a loan may be repaid if a private equity firm sells a company in its portfolio on the secondary market.

Finally, for European insurers, there are considerable advantages of this strategy under Solvency II. The unrated loans, in particular, can significantly reduce an insurer’s Solvency Capital Requirement (SCR), leading to more efficient use of capital and, potentially, higher portfolio returns.

Is this a good time to invest?

Unlike bonds, corporate loans tend to trade close to fair value across the cycle. However, it would be foolish to ignore markets, particularly as Loomis Sayles believes we are currently late in the cycle. This does not mean a downturn is imminent, but that it is likely to occur in the next two to three years.

“We are watching what’s going on with covenants, but we don’t think we are in the danger zone yet,” says Perry. “In any case, financial covenants can blow for a number of reasons. Most are not due to bankruptcy – so we charge a fee to change the covenant and carry on.” Like any credit strategy, corporate loans are sensitive to the default environment. The benign environment in Europe is likely to last for at least two to three years as European economies’growth has just started to speed up, Simon believes. As Loomis Sayles also pointed out, there is no maturity refinancing wall for the next two to three years so the default rate of about 2% should remain steady.

Some investors are concerned about leverage as private equity multiples rise. Over the past 12 months, debt levels have risen to about five times earnings, towards the upper end of historic ratios. However, this concern is mitigated by better-capitalised borrowers than in previous cycles. There is a marked difference, for instance, from the 2005-2007 period and the lead-up to the credit bubble. Private equity funds are now putting larger chunks of equity into deals and many borrowers now come to market with 45%-50% of equity compared to 30%-35% equity in the last market cycle.

Investors should also be reassured by spreads. Spreads are currently 325bps to 425bps, nearly twice the levels of the pre-2007 era. Demand for leveraged loans in Europe current outstrips supply, putting pressure on spreads, but issuance in 2017 is already - 23% up compared with the previous year-so the market is moving into balance.

One potential risk to the European leveraged loans strategy is the Brexit process. If the UK economy suffers as a consequence of the UK’s exit from the EU, UK borrowers will likely suffer too. Natixis AM is keeping a watching brief, prepared to remove UK-sourced loans from its portfolio if the situation dictates. Currently, the direct UK exposure of Natixis AM’s senior secured loans portfolios stands at 4.6% only.

Published in December 2017

Ostrum Asset Management

An affiliate of Natixis Investment Managers

Société Anonyme

Capital €50 434 604.76

Agréé par l’Autorité des Marchés Financiers (AMF) sous le numéro GP 90-009

RCS Paris n°329 450 738

Immeuble Elements

43 avenue Pierre Mendès France

75013 Paris

www.ostrum.com

Loomis, Sayles & Company, L.P.,

A subsidiary of Natixis Investment Managers,

Investment adviser registered with the

U.S. Securities and Exchange Commission

(IARD No. 105377)

One Financial Center,

Boston, MA 02111, USA

www.loomissayles.com

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

Immeuble Elements

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

Natixis Investment Managers Distribution

Natixis Investment Managers S.A branch

RCS de Paris - 509 471 173

Immeuble Elements

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2017 Natixis Investment Managers S.A. – All rights reserved

Private Assets: Making the Retail Revolution a Reality

Private Assets: Making the Retail Revolution a Reality

LTAF Masterclass: Embracing Private Markets in DC Pensions

LTAF Masterclass: Embracing Private Markets in DC Pensions

Loomis Sayles - Investment Outlook - April 2024

Loomis Sayles - Investment Outlook - April 2024

Natixis IM Solutions - Market Review - March 2024

Natixis IM Solutions - Market Review - March 2024