Inflation Linked Income Streams: A good match for fixed income investors' concerns

With interest rates on the rise, it may be surprising to some to learn that real estate and in particular “alternative” property sectors offer income streams linked to inflation at a relatively high yield to fixed income plus underlying capital value protection. But, as Mathieu Cubilié, an Alternatives investment specialist at Natixis IM and Ian Mason, Fund manager at AEW discuss, it is style and performance objectives that will determine which real estate strategy delivers the most benefit going forward.

What is Natixis’s macroeconomic outlook for 2018 and beyond in the UK?

At the start of the year the prognosis for the UK economy seemed to be more of the same, although consensus views on GDP growth were more cautious at c1.5% for 2018. Undoubtedly this view reflects the impact of the ongoing uncertainty of Brexit on business confidence and spending, but consensus also suggests the potential for the UK to rally strongly by 2020 and to even start to outperform both the US and major European economies.

Our view on CPI inflation is that it should have peaked at the end of 2017 and should return to more normal long-term levels as the impact of the fall in sterling washes through the numbers. A note of caution is the extent to which suppliers in the short-term have absorbed higher costs and the extent to which that can continue.

The new dynamic which has now come into the equation is the prospect of rising interest rates as monetary tightening in the USA is starting to influence policies in Europe. Whilst the equity markets’ initial reaction was a fairly dramatic wobble, the prospect of higher inflation driven by growth (rather than rising costs) in the US and UK should not be seen as a threat.

What should we expect from bonds going forward?

Bonds can expect to suffer from the rising rate environment, especially those delivering a fixed coupon and those with a long duration where the expected cash flows will be discounted using higher rates.

Corporate issuers could be hit at some point by tightening credit conditions on more expensive refinancing. Historically, this tends to increase default rates for the weaker companies facing excessively high leverage burdens. This generally occurs after material rate hikes and during an economic slump. But this is far from the Natixis view.

Whilst increasing rates are normal at this stage of the cycle and certainly healthy, especially after such a prolonged period of accommodative policies, we anticipate this should not heavily impact the macro environment. In fact, we think the environment will remain very supportive of the prospects for UK growth.

As usual, the main questions prompted by rates tightening should be about the pace and speed of rate hikes and how central bankers manage market expectations to avoid generating “surprises”. We believe that the recent adjustments have signalled the end to the “bonds bubble” and that the current rates normalisation path will continue. Whilst this does not signal the end of growth, it does mean that there is a lot of capital at risk in cash flow matching strategies. While equity markets might over-react, as it appears they did in February 2018, there are ways for fixed income investors to take advantage of this environment as economies rotate through the growth phase.

Could the real estate asset class really help navigate the current environment?

Real estate fundamentals remain, overall, well oriented to delivering relatively strong returns, and whilst there are variations with regard to sector and geography, AEW particularly sees opportunity in property assets beyond shops, offices and industrial, (also known as “alternative” sectors). For existing, particularly regional occupiers, it seems to be “business as usual”, despite Brexit. This means good return opportunities should continue to arise from specific sub-sectors and from skilful stock selection. There is also an absence of excessive stock due to constraints on development which supports rental value growth.

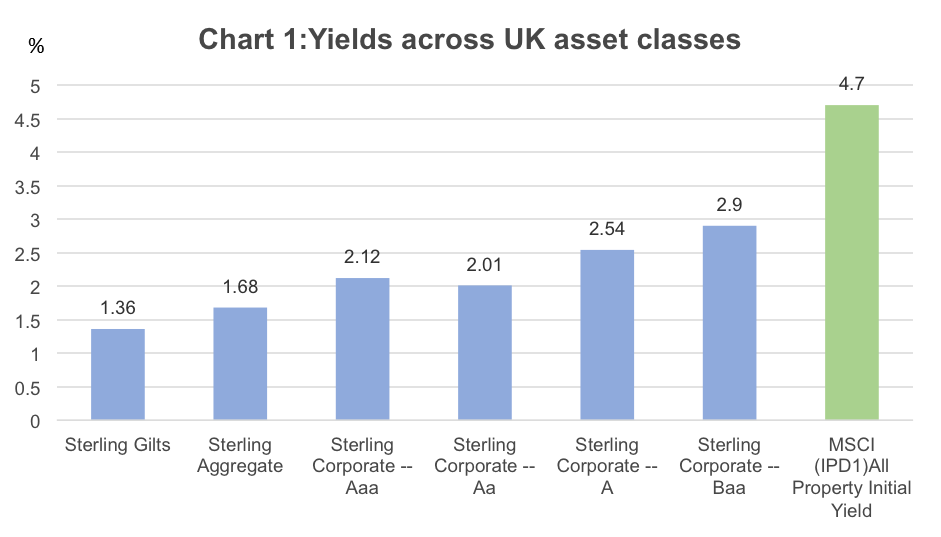

Rising rates and inflation can benefit real estate. In general terms, real estate values have increased in an environment of yield compression as multi asset investors seek higher yielding assets. Whilst these capital gains are expected to slow going forward, income levels are expected to remain at a substantially higher level than what most UK fixed income sectors can deliver, as shown in Chart 1 below.

Source: BarCap.com, MSCI1. April 2018

This next stage of the cycle should drive the income component of returns. For Real Estate, income comes through as higher market rents are driven by occupier demand, as well as from occupiers who prefer their rental liabilities linked to inflation. Leases of this nature tend to be found in the “alternative” property sectors, including acyclical sectors (such as healthcare and senior living),which are driven less by economic growth and more by demographics. This is also the case in the regional UK markets, which have not suffered the excesses of investor demand experienced in Central London and the South East.

It is possible to invest in real estate assets with the aim to deliver higher income than most available strategies in the market with a very high level of cash-flow predictability while still benefiting from diversification. Such characteristics can be of great interest for clients in need of predictable and secure revenue streams to match their liability requirement.

How does this translate in bond terms?

Taking a fixed income investor’s perspective, core real estate strategies can be modeled as a bond. More precisely, they can be considered as credit bonds delivering a variable coupon with several components:

| Variable rate | In relation with the average lease duration |

| Inflation indexation | Where rents are linked to CPI/RPI |

| Risk premium | Reflecting tenants’ quality and underlying assets’ quality |

So, where are higher income/inflation linked income streams found in real estate?

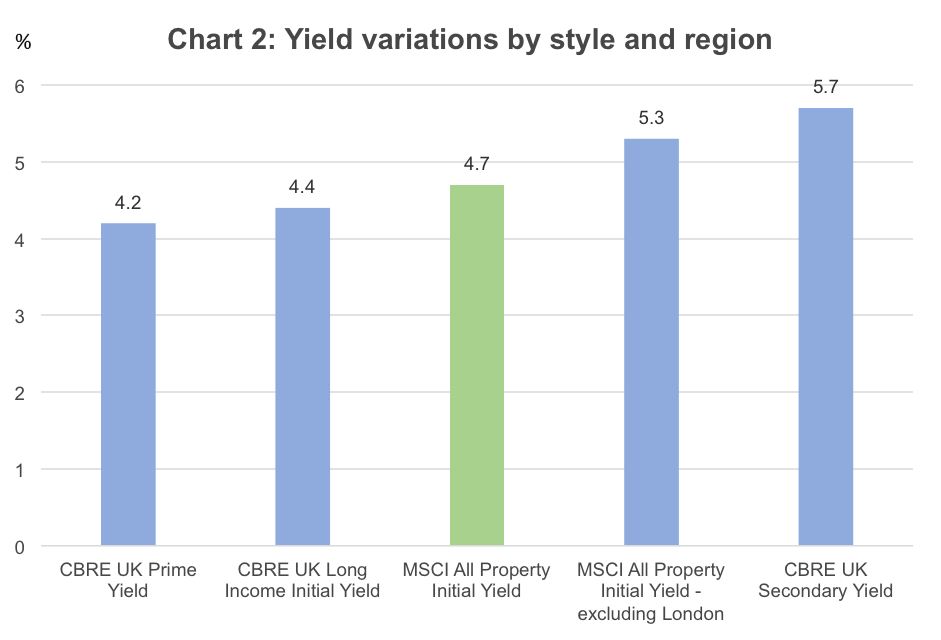

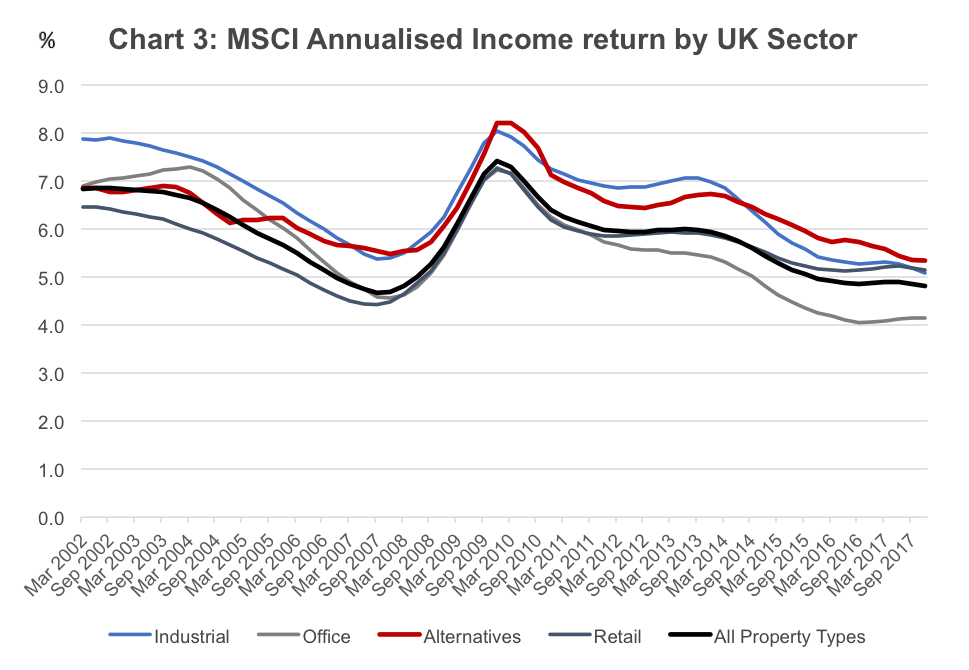

Any property expert will tell you that the characteristics of real estate assets vary greatly depending on the sector and more particularly on the style of property, as Charts 2 and 3 illustrate.

Source: CBRE, MSCI 2018

Traditionally, it has been a manager’s sector weightings that have been the main way to differentiate one real estate fund from another. Even though weightings against a typical IPD relative return benchmark tend to be similar, different sectors have markedly different prospects. In AEW’s view:- Retail is a low yielding sector with less interest currently. It is suffering from the impact of e-tailing.

- London City offices is another sector to avoid given the high reliance on financial services tenants whose future is uncertain due to Brexit.

- In contrast, we favour alternative sectors like care homes and nursery schools where strong occupier demand is driven far more by acyclical trends like demographics and social need. Most other real estate strategies tend to focus on shops, offices and industrial and are more sensitive to economic volatility than alternative sectors.

Source: MSCI, December 2017

Traditionally, institutional core real estate strategies have focused on delivering relative total returns or absolute total returns in the case of Value-Add and Opportunistic programmes. This has meant that real estate has usually been allocated to the investors’ “growth” bucket, along with equities where less focus was given to the fact that over the last 30 years 70-80% of UK real estate’s return came from income. In the years following the Global Financial Crisis, as bond yields fell and the hunt for higher returns began, Long-Lease real estate funds were launched as a stable cash-flow product. However, these are structured, managed and priced as bond proxies, typically with cash plus or gilts plus targets, rather than playing to the strengths of real estate as a Real Asset.

Neither of the above two approaches focus on delivering high income, principally because of the way in which their performance is benchmarked:

- In the case of core strategies, relative return objectives do little to help align investors who want to maintain steady dividends and capital preservation. The focus on total return rather than income tends to produce unattractive levels of volatility for many investors focused on cash flow matching.

- The total return objective of long-lease funds offers little alignment with investors needing a relatively high level of stable, secure cash-flow. For such strategies, higher rates necessitate capital loss at some point.

- Focusing on delivering a high and secure income through core assets provides a very different investment outcome. Income has proven to be much more stable over time than total return, therefore focusing on delivering high, predictable income reduces volatility due to yield impact.

Does focusing on Real Estate income mean taking more risk?

Achieving a higher income yield than fixed income is traditionally thought of as only being achieved at the cost of taking more risk, however this is not necessarily the case for a strategy that effectively redefines property as a Real Asset.

How do the risks compare at a point in the cycle where bond yields are starting to rise and long-lease strategies are likely to either fall in value or have their risk premia squeezed? The choice is either buying arguably over-priced assets where income is ruled by the bond market, or investing in assets providing income secured on core quality property in alternative sectors and locations that are in demand from occupiers and for which there are real prospects for growth.

Investors looking for income might be interested in considering a property strategy that targets real total returns as its performance objective. This strategy is driven by income targets from rents secured on property fundamentals that meet the changing demands of the real economy. It is also a strategy that offers clear alignment between the fund manager and the needs of investors, as well as a foot inside both equity and bond camps: a real asset growth strategy with relatively high levels of sustainable income as the hunt for yield continues.

Published in May 2018

AEW Europe

Subsidiary of Natixis Asset Management Group

Privately-held French Société anonyme à conseil d’administration.

RCS Paris B 409 039 914

8-12 rue des Pirogues de Bercy

75012 Paris

France

www.aeweurope.com

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2018 Natixis Investment Managers S.A – All rights reserved

2018 European Property Market Outlook

2018 European Property Market Outlook

Real Estate Alchemy

Real Estate Alchemy

Loomis Sayles - Investment Outlook - April 2024

Loomis Sayles - Investment Outlook - April 2024