Five Myths About U.S. Large Caps

Key Takeaways:

- The world always seems risky and large-cap stocks often appear to be in the firing line. Yet the facts do not bear out the fears.

- Active managers with high active share and longer holding periods can significantly outperform the S&P 500®.

- A longer-term time horizon can appeal to investors worried about geopolitical events because the impact tends to have little effect on the long-term growth of markets.

- Ultimately, good companies will do well and provide strong returns to their shareholders – poor companies will lose money and value.

Resources

Sceptics have put forward five broad arguments against active investment in the largest U.S. companies:

- They are best suited solely for passive investment

- There is too much competition for assets

- Large caps are too expensive

- The market is too uncertain

- U.S. large caps are less interesting than other markets

#1 The U.S. large-cap market is best suited for passive

A common investor view is that in a mature market, such as U.S. large caps, there is little point in trying to beat the index. The market, so the argument goes, can never embed all information, but it is sufficiently efficient that passive investing offers the best value. Since active strategies underperform in aggregate after fees are deducted, they should be avoided when investing in mature markets.

The evidence, however, does not favour this viewpoint.

This theory is little different than asserting that because the average of all the sports teams in a league is 0.500 (an equal number of wins and losses) over the course of a season, there is no way to tell which team can outperform. This is patently untrue. More talented players, a winning philosophy, investment in player development and the depth of the squad can all be strong predictors of which teams will fare well and which will disappoint.

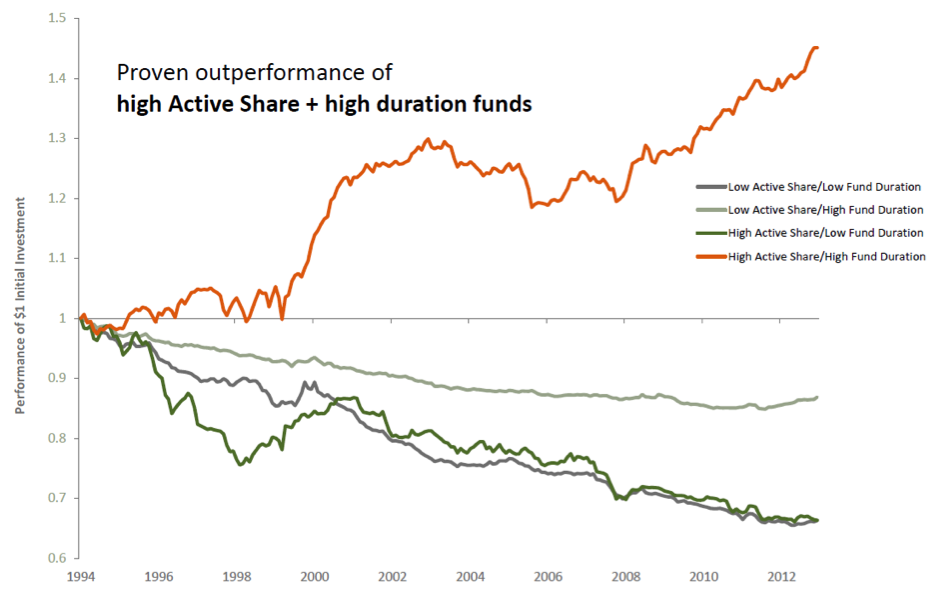

Similar predictors of success can be found in investment management. There is strong and independent evidence that truly active managers can outperform in U.S. equities. Managers who have high active share (deviation from the index) and hold stocks for the long term can be shown to significantly outperform the S&P 500®.

Active managers can outperform in U.S. equities

High Duration = holding period of more than 24 months

Low Duration = holding period of less than 7 months

Source: Martijn Cremers & Ankur Pareek “Patient Capital Outperformance: The Investment Skill of High Active Share Managers Who Trade Infrequently.” September 2014.

As the graph indicates, returns by managers with high active share and long duration (long portfolio holding times) return, on average, nearly 1.5 times more than the index. Investment funds that are closet indexers, on the other hand, significantly underperform.In short, investment houses with the conviction to be active and patient investors can substantially outperform passive investments.

#2 The U.S. large-cap market is too competitive

It’s undeniably true that more analysts and portfolio managers are looking under the hood of the U.S. large-cap market than any other market in the world. Each hopes to find the opportunity that creates value that no one else has yet identified.

In the past, simple value screens, such as low price-earnings (PE) ratios, were used to identify value. These screens are still used, but have much less predictive power. In the wake of more competition, the traditional value metrics have underperformed for more than a decade now.

Increased competition is no reason to abandon the search for value, however. At Harris, we have developed an investment philosophy that has three distinct value-creating elements, which allows us to be flexible with our definition of value:

- The first is to buy companies only when they are priced at a large discount to the firm’s estimate of intrinsic value. These estimates are based on fundamental research rather than multiples of ratios. This large discount means that a bad call results in only small losses, but a good call can lead to substantial returns.

- The second is to avoid value traps, which can result in cheap companies becoming even more so because their fundamentals just never improve. A number of loss-making technology companies fall into this category. At Harris, we look for companies where earnings per share are growing significantly faster than the overall S&P 500®.

- The third is to invest in companies where the interests of the management team are aligned with shareholders. Aligned management teams tend to own plenty of stock or options and have incentive plans that pay out on metrics that drive business value. Incentive plans based on return on capital or a per share metric are more aligned than incentives based on hitting certain sales or income targets.

#3 The U.S. large-cap market is too expensive

Many investors are starting to question the longevity of a market recovery that has lasted nearly a decade.

The duration of the recovery is longer than economic recoveries of the past, but that ignores its magnitude. Magnitude creates excessive valuations that are then vulnerable to corrections. But the current recovery has produced GDP expansion of just 2% a year on average, which is barely trendline growth.

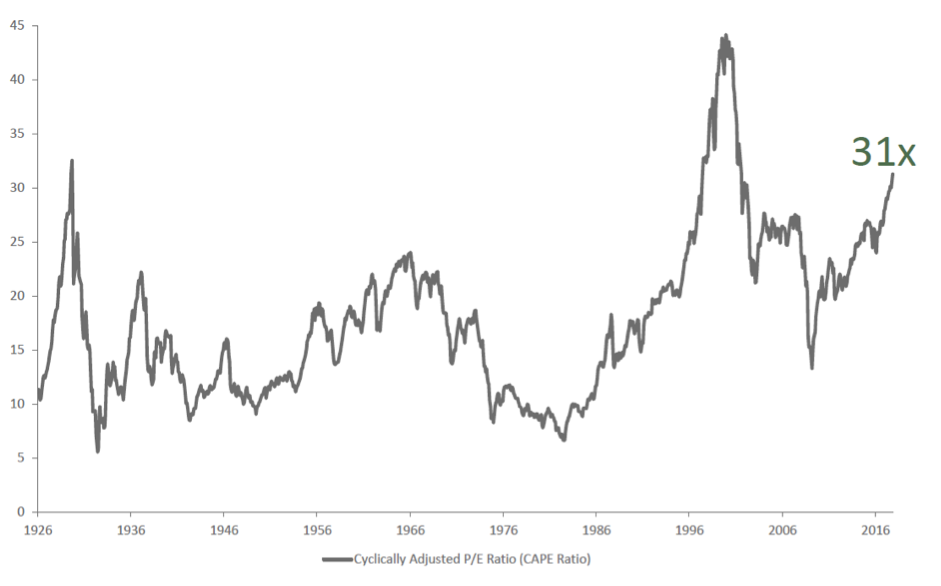

Price versus earnings expectations for the next year are in a range of about 15-17x earnings, which historically has produced good annual equity returns and a significant premium to bond returns.

Shiller P/E Ratio for the S&P 500® Index (1926 –2016)

Source: www.mltpl.com/shiller-pePrice earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio), Shiller PE Ratio, or PE 10.

If we look at industrial companies like automotives, which are selling at mid-single digit multiples, they are in better shape than a decade ago, with better management structures and more cash generation. These kinds of firms have huge potential to take advantage of the growth of the middle classes in developing markets.#4 The U.S. large-cap market is full of uncertainty

Seemingly every year a new concern arises that has investors reaching for the sell button. Fears over the sustainability of global equity markets have arisen many times in the past: 9/11, the high-tech boom and bust, the Iraq wars, the Lehman Brothers collapse, and the eurozone crisis.

The world always seems risky and large-cap stocks often appear to be in the firing line. But the facts don’t bear out the fears. Notwithstanding these negative events over the last two or three decades, total returns from the S&P 500® have increased investors’ wealth by 11 times (from 1991 to 2017). Investors who tried to time the market but reduced their allocations to large caps at times of geopolitical worry may have given up significant value.

Even better returns are possible using an active manager with high active share and plenty of patience. At Harris, we are bottom-up value investors who ignore macroeconomic noise. We look solely at the fundamental attributes of companies rather than try to compete on the basis of superior economic views.

We are concentrated investors. We do not dilute our portfolios with overdiversification, leading to portfolios of perhaps 50 companies rather than 100-2,000.

We are patient investors. Our aim is to hold these companies as long as they appear undervalued, with our analysts making projections for business fundamentals over multi-year periods rather than for the next quarter or year. This is a long analytical timeframe compared to other public market investors and is more akin to a private equity approach. We believe this long-term time horizon is appealing to investors worried about current geopolitical events because the impact tends to be short term and have little effect on the long-term growth of markets and profits.

#5 The U.S. large-cap market is less interesting

The U.S. large-cap market can appear dull compared with fast-growing emerging markets. Why, investors reason, should we accept unexciting returns when other markets hold out more promise?

Well, firstly, GDP expansion in a country doesn’t always translate into rising share prices. Secondly, that exciting-looking growth comes at the price of quite considerable volatility. Thirdly, and perhaps most importantly, a very sizeable chunk of the revenues of U.S. large caps are sourced abroad. With global exposure, U.S. large caps can take advantage of fast-growing regions, while investors have the comfort of knowing these sales are being carried out by established and reputable organisations.

To identify companies that can benefit from overseas growth requires deep resources and experienced global investment teams. The companies on our approved list are all vetted by our experienced U.S. and international investment committees. Our analysts hold more than 1,500 onsite management meetings every year to assess business and management quality, which results in 300-400 stocks it believes are of sufficient quality to meet the analysts’ definition of intrinsic value.

Conclusion – less worry, more skill

Worrying is normal. We need to worry to survive. But we also need to set our worries into context. Despite investors’ concerns about markets, they should be aware that these are probably pretty normal times. Good companies will do well and provide strong returns to their shareholders, and poor companies will lose money and value.

The key to investing in any market is to employ skill and patience to tease out the many opportunities that exist.

Harris Associates

An affiilate of Natixis Investment Managers.

Investment adviser registered with the U.S. Securities and Exchange Commission (IARD No. 106960), which is licensed to provide investment management services in the United States.

The company conducts all investment management services in and from the United States.

Two North LaSalle Street, Suite 500

Chicago, Illinois 60602, Etats Unis

www.harrisassoc.com

Natixis Investment Managers

RCS Paris 453 952 681

Share Capital: €178 251 690

43 avenue Pierre Mendès France

75013 Paris

www.im.natixis.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

Copyright © 2018 Natixis Investment Managers S.A. – All rights reserved

How to Assess How Active a Portfolio Is?

How to Assess How Active a Portfolio Is?

Passive is Good for Active

Passive is Good for Active

Loomis Sayles - Investment Outlook - April 2024

Loomis Sayles - Investment Outlook - April 2024

Natixis IM Solutions - Market Review - March 2024

Natixis IM Solutions - Market Review - March 2024