Welcome to the Meh Market

Results from the 2019 Natixis Midyear Strategist Survey suggest that outcomes will be more muted as markets grapple with a number of downside scenarios and little in the way of upside surprises. Among the 17 respondents representing Natixis Investment Managers, its affiliated investment managers, and Natixis Bank, few are optimistic. The strategists largely see lackluster equity returns after the first half’s extraordinary run, as well as continued modest downward pressure on sovereign bond yields. With little to be excited about, this remarkably consistent outlook may be best summarized by one word: “Meh.”

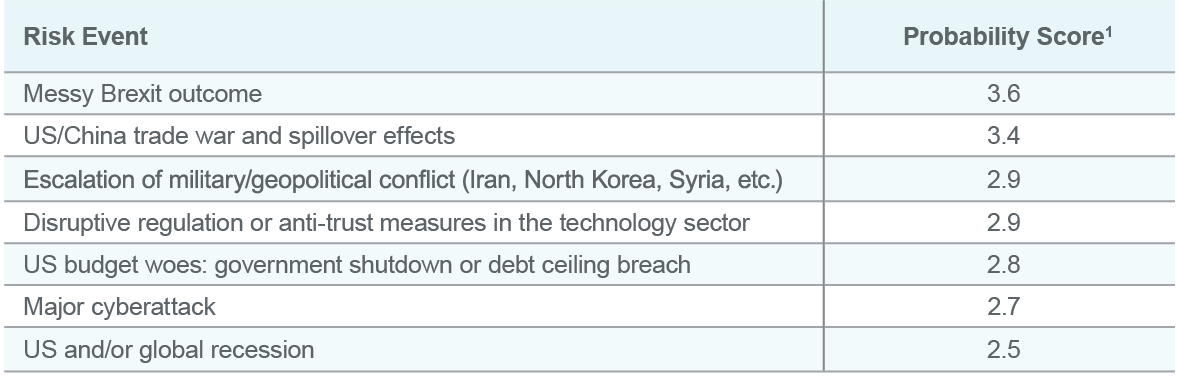

Plenty of downside risks

In terms of risk, Natixis strategists cited a messy Brexit as the most likely downside scenario – not surprising given the growing political uncertainty in the UK. Not far behind on the list are the spillover effects from a US/China trade war. With China’s economy growing at its slowest rate in 27 years, concerns here appear to be well founded. However, in a world where the “R-word” seems to be cropping up with more frequency, respondents were much less concerned with the possibility of recession. They cited “a US and/or global recession” as the least likely downside scenario in our question about potential risks.

Worried about Brexit but not recession

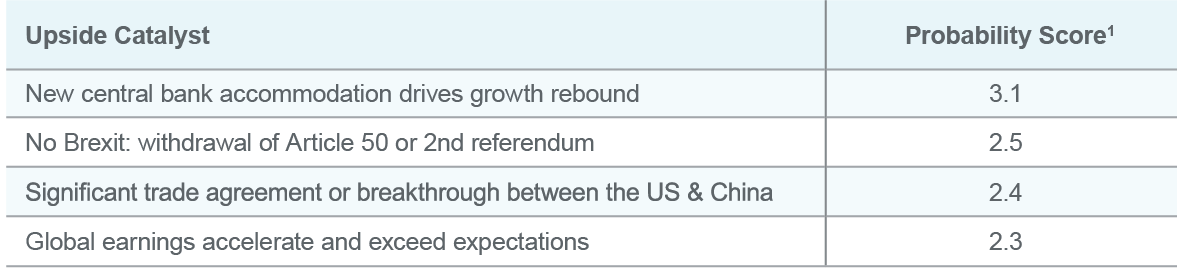

More telling though, may be the strategists’ general lack of enthusiasm for the upside potential. While some hold hope that new central bank accommodations could drive a rebound in growth, just as many believe it is unlikely to work. Few anticipate any positive Brexit scenarios. Likewise, they are neutral to negative on prospects for a significant breakthrough between the US and China on trade. More significantly, they do not foresee accelerating global growth or equity earnings in the next six to 12 months. “The survey results clearly show that, in aggregate, our respondents don’t see a lot of positive market catalysts on the horizon – nor do they see a recessionary worst-case scenario as very likely in the near term. It’s kind of a ‘muddle through’ outlook”, noted Esty Dwek, Head of Global Market Strategy, Dynamic Solutions, Natixis Investment Managers.

Few upside surprises expected

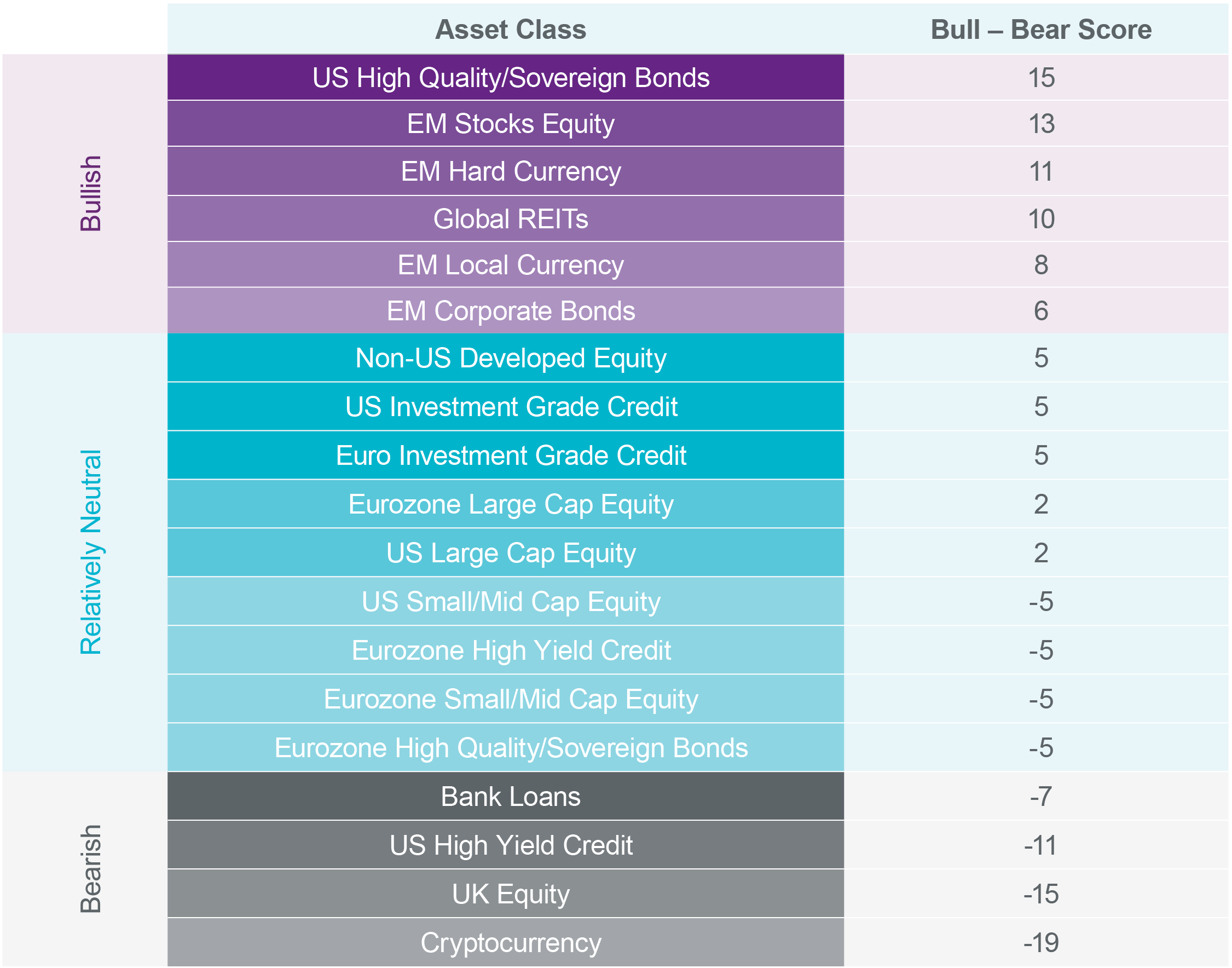

With a strong expectation of Fed rate cuts on the horizon, Natixis strategists are most bullish on US Sovereign bonds, followed by emerging market equities, global REITs, and emerging market bonds of all flavors (hard currency, local currency, and corporate). The common thread running through these bullish forecasts is accommodative central bank policy and ample global liquidity. In turn, they are most bearish on cryptocurrencies, UK stocks, US high yield, bank loans, and European sovereign bonds. The dichotomy between US and European high quality/sovereign bonds was striking in an environment where US bond yields are significantly higher and seen as having much more room to fall.

Weighted Net Bullish – Bearish Score2

Natixis strategists predict little in the way of equity returns in the US and Eurozone over the next six to 12 months. But that’s not to say the consensus calls for dramatic losses either. Overall, the outlook on equities is balanced and no strategists forecast a bear market (-20%) or even a market correction (-10%) in this time frame. In short, they think the bull run may stall in the near term – but not falter significantly.

Overall, they are relatively neutral on small-, mid-, and large-cap stocks, but respondents do see the potential for S&P 500 performance to tail off in the coming months. Given the index delivered 17% returns through the first half of the year, projections for flat to slightly lower performance through year end still presents a solid counterweight to 2018’s losses.

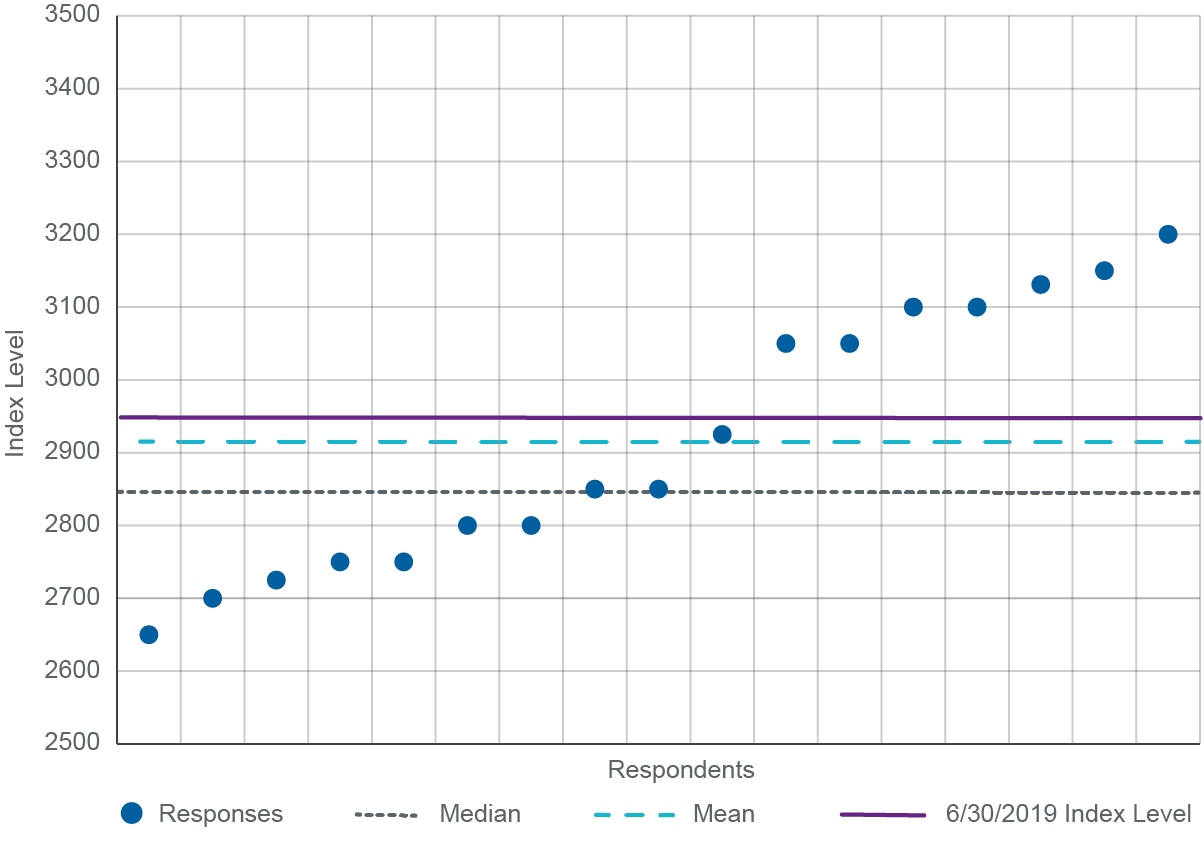

In focus: S&P 500®

Source: Natixis Investment Institute, Bloomberg, June 30, 2019.

On average, Natixis strategists project the S&P 500® will close out the year at 2,916.53, or -0.86% lower than where it stood on June 30. Even here, Natixis strategists presented a tight range of views, calling for returns between 8.8% and -9.9%, with the median at -3.1%, which would add up to a net 14% gain for the year.

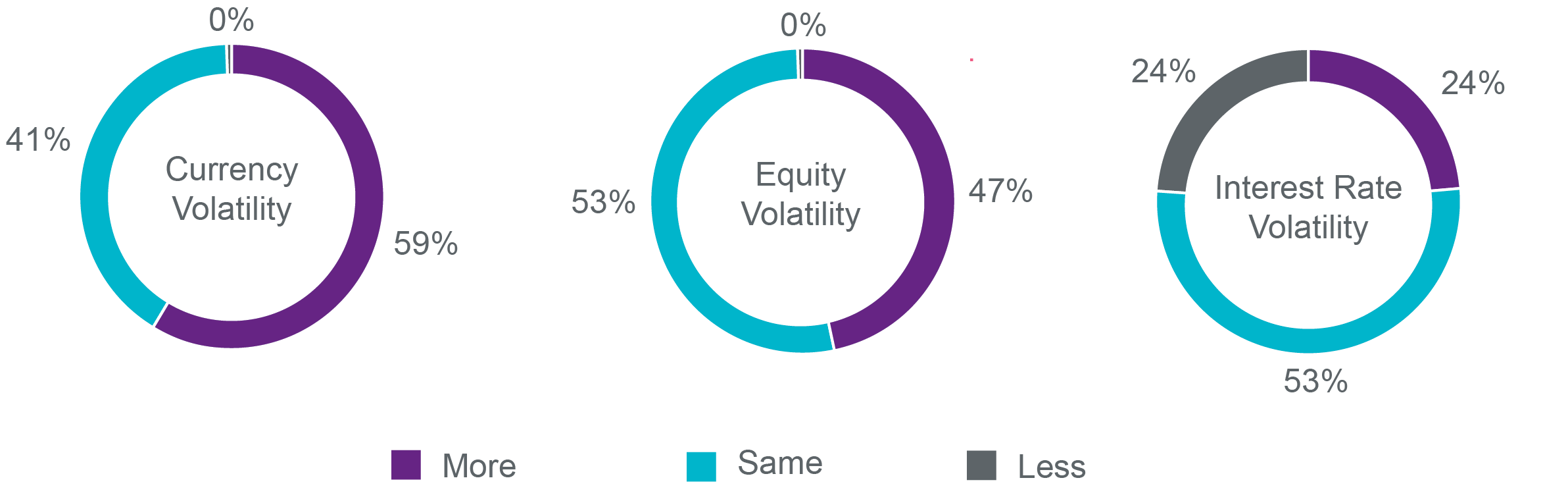

Natixis strategist projections for volatility go hand-in-hand with their equity outlook. Overall, they anticipate a slight increase in volatility with the VIX rising 2.1 points from its mid-year level of 15.1. This average projection to 17.2 represents a modest but meaningful increase in volatility overall. Across broad assets, and in contrast to recent market readings, the respondents saw currency volatility picking up the most, followed by equity volatility, with bond/interest rate volatility likely to move the least. The results were clearly skewed to a somewhat higher volatility regime in the coming year with none of our 17 strategists forecasting “lower volatility” for either equities or currencies.

Volatility Expectations

Sentiment for the US falls in line with broader views on global equity markets with Natixis strategists calling for modestly higher levels of volatility.

On the bond side of the equation, central banks continue to be the focus as Natixis strategists anticipate more dovish policy from both the Federal Reserve and the European Central Bank (ECB).

Some may be surprised that the Fed would consider rate cuts at a time when the S&P 500® is near all-time highs and unemployment near all-time lows. However, the markets are clearly pricing in rate cuts and our Natixis strategists agree with market sentiment. On average, they predict the Fed will ease rates back by 50 basis points by year end, with all but one respondent forecasting at least one cut.

In Europe, respondents see further easing from the ECB and anticipate a 5-10 bps reduction in the overnight deposit rate. Consensus is not as strong on ECB cuts, as almost half (8 out of 17) forecast no change to the overnight deposit rate. This may indicate that rather than reducing rates the ECB may first try other levers such as offering additional forward guidance, restarting large-scale asset purchases (QE), or tiering the deposit rate.

While rate cuts are anticipated on both sides of the Atlantic, Natixis strategists share a split view on bonds. Among all asset classes, the strategists are most bullish on US High Quality Sovereign Bonds, calling for the US 10-Year Treasury to rally by 10 bps to finish the year near 1.90% (vs. 2.01% at mid year).

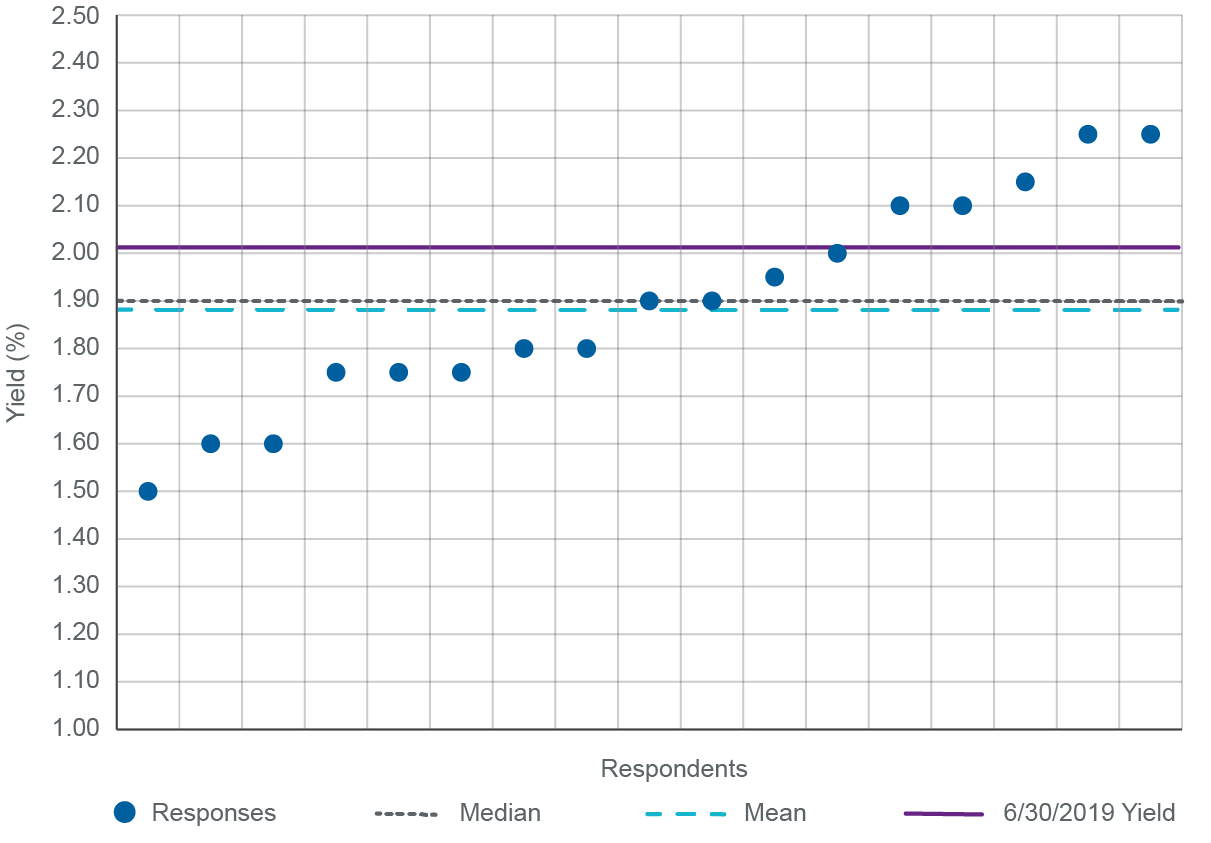

In focus: 10-Year US Treasury Yield

Source: Natixis Investment Institute, Bloomberg, June 30, 2019.

On average, Natixis strategists estimate 10-year treasuries will yield 1.89%, a 12 bps decline from where they ended on June 30. Estimates ranged from 1.50% to 2.25% among respondents with those forecasting lower rates outnumbering those calling for higher rates by a two-to-one margin. Only one strategist called for rates to remain unchanged.

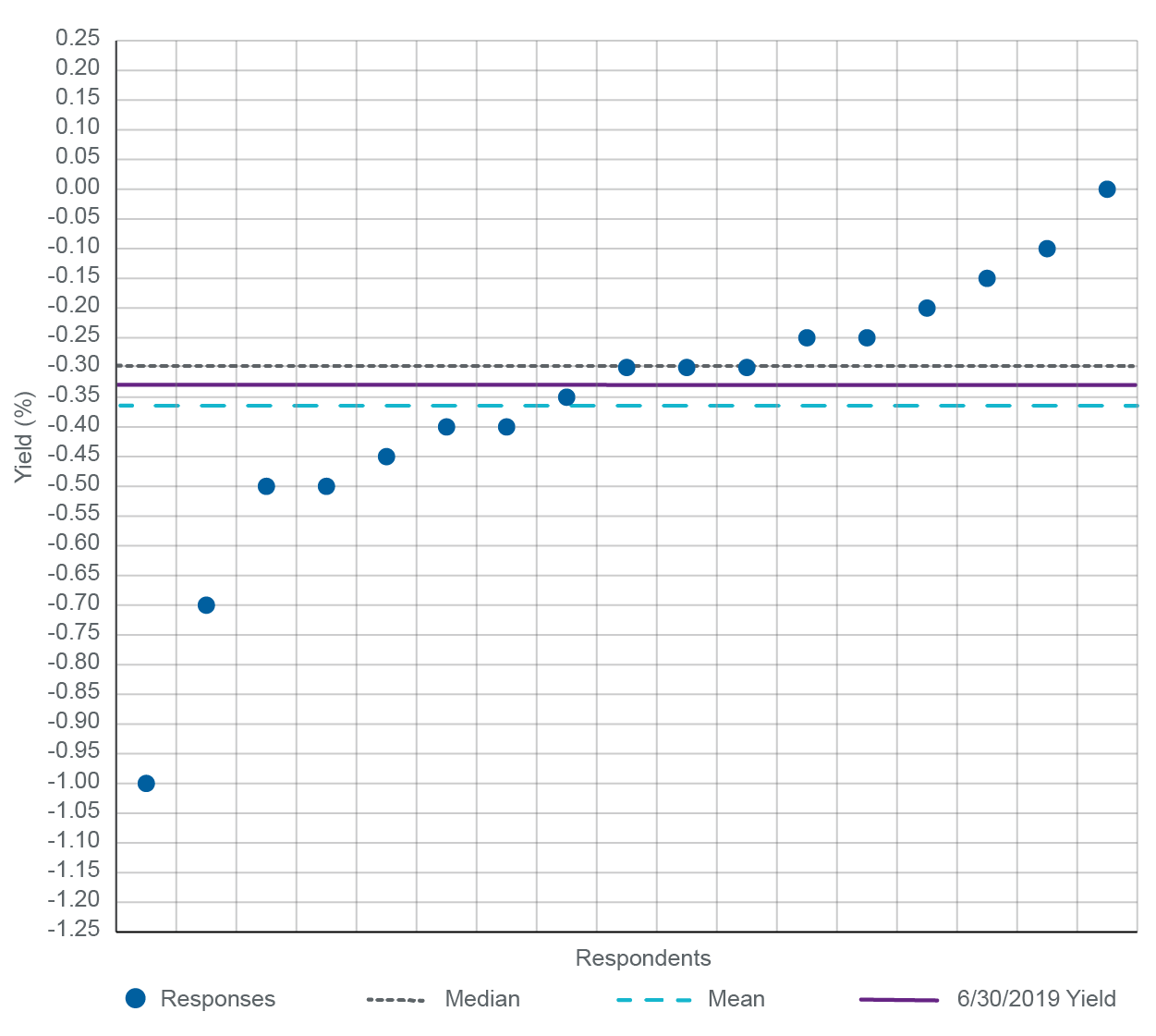

In focus: German 10-Year Bund Yield

Source: Natixis Investment Institute, Bloomberg, June 30, 2019.

While the high to low range for the Bund ran from 0.00% to -1.0%, Natixis strategists forecast little or no change, on average, through year end. In what could best be termed apathetic with a bearish skew, our respondent pool included just two bulls, seven bears, and eight neutral.

The trend toward more dovish interest rate policy from the Fed and ECB are pronounced in strategist sentiment on currency. Overall expectations for volatility run strongest here with 10 of 17 forecasting increased currency volatility and no one anticipating any declines.

- Euro vs. Dollar With an average year end estimate of 1.131 compared to 1.137 on June 30, strategists see the euro roughly unchanged vs. the US dollar. Despite the small decline, the range of estimates was fairly wide with the highest calling for 1.20, a 5.5% increase, and lowest anticipating 1.05, or a 7.7% decline.

- GBP vs. Dollar Forecasting continued weakness on the back of little Brexit clarity and a growing likelihood of a “no deal” outcome, strategists see the pound sterling weakening 1-3% vs. the US dollar on average. The spread of estimates among Natixis strategists was fairly wide, ranging from 1.10 (-13.4%) to 1.30 (+2.4%), but was clearly skewed toward sterling weakness.

- Yen vs. Dollar Strategists also see the yen weakening slightly against the USD through year-end. Despite estimates ranging from 100.0 (-11.3%) to 120.0 (+7.3%), respondents predict a -0.3% decline from 107.9 to 108.2 on average. Sentiment was also skewed bearish with 10 of 17 calling for a weaker yen.

In recognition of potentially lower rates and/or its defensive properties, gold rose by 10% in the month prior to fielding our survey. In contrast our strategists, on average, see the gold rally stalling, with prices down by 1%-3% by the end of 2019. Excluding outliers, the low-to-high range ran from $1,200 to $1,525 against $1,410 at June 30. Sentiment was split evenly with eight calling for gold to be higher in the next six months and nine calling for it to be lower.

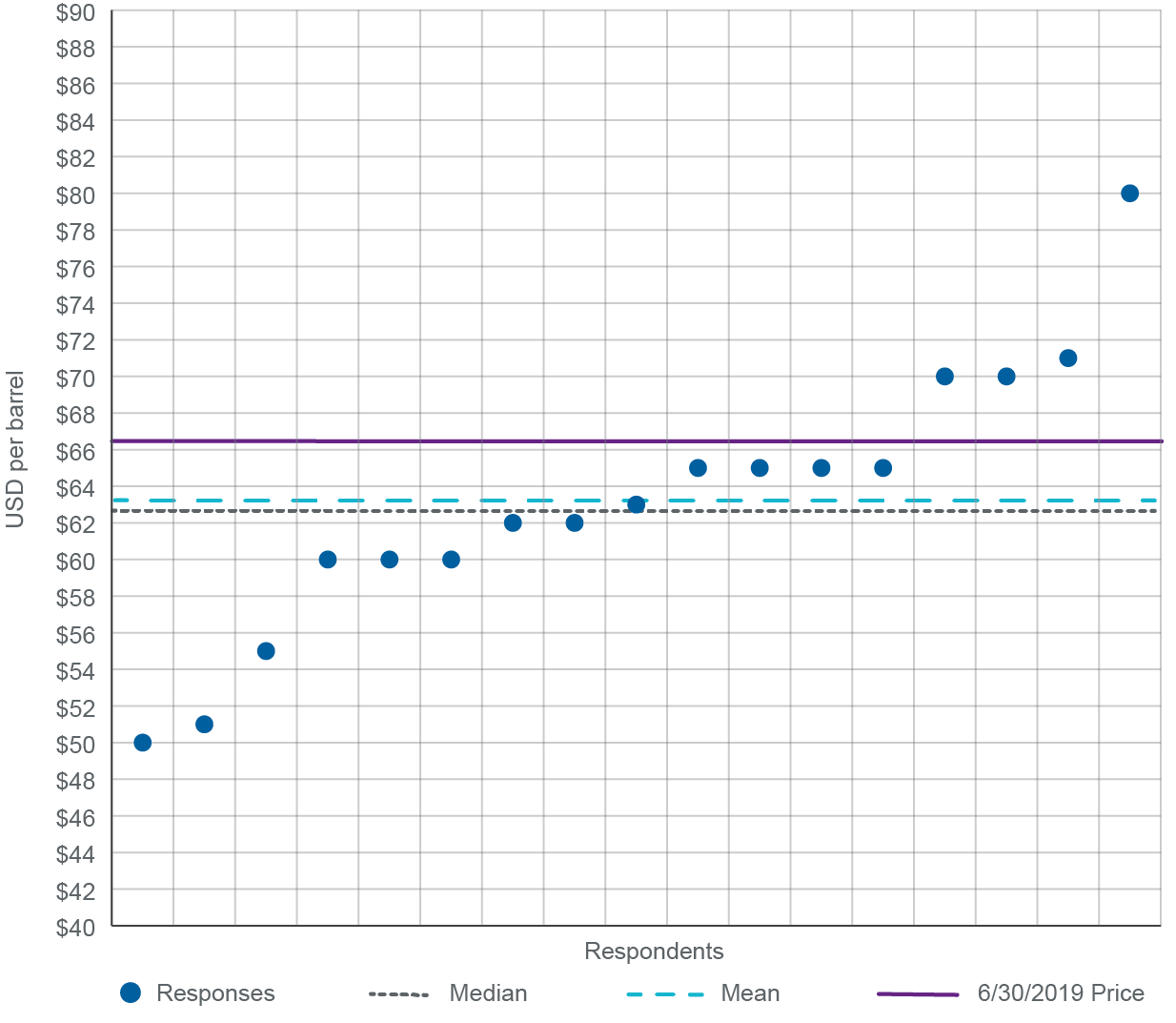

Brent Crude

With Brent Crude at $66.55 per barrel on June 30, Natixis strategists expressed a slightly bearish view on oil, predicting a modest 5.1% decline to $63.18 by year end. Sentiment was significantly skewed downward, with nine calling for lower prices, four calling for higher, and the same number seeing no change. Excluding one upside outlier, the low-to-high range ran from $50 per barrel (-25%) to $71 (+12%).

In focus: Brent Crude

Source: Natixis Investment Institute, Bloomberg, June 30, 2019.

Strategists were split on the direction for Brent Crude oil, but it slightly skewed to lower prices.

After a dismal end to 2018, equities and bonds rallied in the first half of 2019. Performance to date has been driven largely on the hopes of new rounds of central bank easing. But as what the market hoped for comes closer to reality, market strategists within the Natixis Investment Managers family find little to get excited about. Perhaps the best news is that despite projections for lackluster performance, they are not calling for a dramatic retreat from the impressive gains. After stinging losses in Q4 2018, maybe “meh” is something to be excited about after all.

About the Survey

The Natixis Midyear Strategist Survey is based on responses from 12 representatives across eight of Natixis’ affiliated investment managers, three representatives from three operating groups at Natixis Investment Managers, and two representatives from Natixis Corporate & Investment Banking (CIB):

- Michael J. Acton, CFA®, Director of Research, AEW

- Axel Botte, Global Strategist, Ostrum Asset Management

- François-Xavier Chauchat, Chief Economist and member of the Investment Committee, Dorval Asset Management

- Esty Dwek, Head of Global Market Strategy, Dynamic Solutions, Natixis Investment Managers

- James Grabovac, CFA®, Investment Strategist, Municipal Fixed Income team, Loomis Sayles

- Jack Janasiewicz, CFA®, Senior Vice President and Portfolio Strategist, Natixis Investment Managers

- Brian P. Kennedy, Portfolio Manager, Full Discretion Team, Loomis Sayles

- Mathieu Klein, Chief Investment Officer and co-founder, Darius Capital Partners

- Ibrahima Kobar, Deputy Chief Executive Officer, Global CIO, Ostrum Asset Management

- David Lafferty, CFA®, Senior Vice President and Chief Market Strategist, Natixis Investment Managers

- Joseph Lavorgna, Chief Economist, CIB Americas, Natixis

- Maura Murphy, CFA®, Portfolio Manager, Alpha Strategies team, Loomis Sayles

- Jens Peers, CFA®, CEO and CIO, Mirova3

- Dirk Schumacher, European Head of Macro Research, CIB, Natixis

- Hans Vrensen, CFA®, MRE, Managing Director and Head of Research & Strategy, AEW Europe

- Philippe Waechter, Chief Economist, Ostrum Asset Management

- Chris D. Wallis, CFA®, CPA®, CEO, CIO, Senior Portfolio Manager, Vaughan Nelson Investment Management

2 Weighted sum of bullish responses (>5) minus bearish responses (<5) for each asset class based on a 1-10 scale (1 = most bearish, 10 = most bullish) with 5 being neutral.

3 Mirova is operated in the US through Mirova US LLC (Mirova US). Prior to April 1, 2019, Mirova operated through Ostrum US.

Past performance is no guarantee of future results.

All data as of June 30, 2019 unless noted otherwise.

The S&P (Standard & Poor’s) 500 Index is an index of 500 stocks often used to represent the US stock market.

The CBOE Volatility Index (the VIX) measures the implied volatility of the S&P 500® Index. The VIX is quoted in percentage points and represents the expected range of movement in the S&P 500 index over the next year.

Quantitative easing (QE), also known as large-scale asset purchases, is a monetary policy whereby a central bank buys predetermined amounts of government bonds or other financial assets in order to inject liquidity directly into the economy.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

All investing involves risk, including the risk of loss.

You cannot invest directly in an index.

This material is provided for informational purposes only and should not be construed as investment advice. The views and opinions expressed are as of July 19, 2019 and may change based on market and other conditions. There can be no assurance that developments will transpire as forecasted, and actual results may vary.

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis”) and does not sponsor, endorse or participate in the provision of any Natixis services, funds or other financial products.

The index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

2649744.1.1

All back to bonds?

All back to bonds?

Why Everyone’s Talking About… Market Bubbles

Why Everyone’s Talking About… Market Bubbles

Equities: How worried should we be about valuations?

Equities: How worried should we be about valuations?

Global Corporate Bonds – Attractive Yields but Thin Risk Premium

Global Corporate Bonds – Attractive Yields but Thin Risk Premium